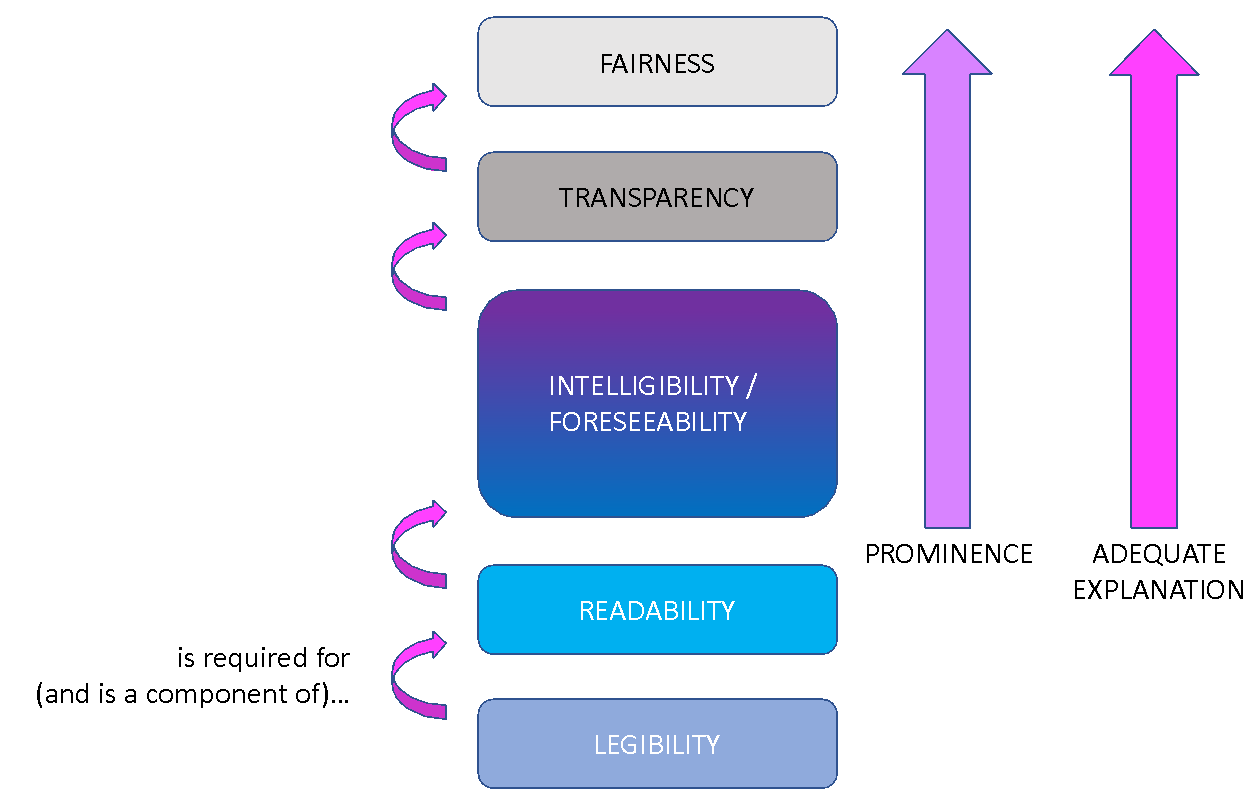

what they mean, why they differ, and how to measure them

The legal basis, the FCA's position, and why readability scores alone create compliance risk under Consumer Duty

Introduction

What this article covers: the legal definition of intelligibility, how it differs from readability in law and practice, the six drivers of complexity readability frameworks miss, and how to measure intelligibility to FCA Consumer Duty standard.

Most regulated firms test their communications for readability. Many believe that a good Flesch-Kincaid score is evidence of consumer understanding. The FCA has been explicit: it is not. The Consumer Understanding Outcome under Consumer Duty requires firms to evidence intelligibility - a legally defined concept that goes far beyond word length and sentence structure.

This article explains the distinction, its legal grounding, and what genuine intelligibility measurement requires. For context on the Consumer Duty framework itself, see: What is the FCA Consumer Duty?. For how this distinction applies to AI-generated content, see: AI-generated content and FCA compliance.

The legal distinction: intelligibility vs readability

What intelligibility means in law

The legal definition of intelligibility has been shaped by Court of Justice of the European Union (CJEU) case law, most significantly around the time the Consumer Rights Act 2015 came into force. Intelligibility means more than simply being capable of being understood. The legally operative definition, directly relevant to the FCA Consumer Duty, is:

LEGAL DEFINITION

"Able to be understood by the target audience, including the context, the relevance, and the consequences of the information for the reader." CJEU case law on consumer contracts; reflected in the Consumer Rights Act 2015

This definition has three components, each of which readability frameworks fail to assess:

- Content understanding: the reader can understand the language and concepts being used

- Contextual relevance: the reader understands how the information applies to their situation

- Consequential understanding: the reader can understand the potential economic consequences, risks, rights, and obligations, what the CJEU defines as foreseeability

Intelligibility and foreseeability: the linked concepts

Since the relevant CJEU rulings, the definition of intelligibility has been explicitly linked to the concept of foreseeability - long established in other areas of law (foreseeable harm, for example). Applied to consumer communications, foreseeability means that the average consumer must be able to understand the "potentially significant economic consequences" of the terms of a contract. This includes their rights and obligations, and the risks they face.

Intelligibility and foreseeability are intrinsically linked: each necessary for the other. A communication that is technically intelligible (all words understood) but fails to convey the consequences of the contract is not foreseeable, and therefore fails the legal standard. This is the dimension most completely absent from readability frameworks.

What readability means in law

By contrast, readability is not clearly defined in law. The nearest legal concepts are "plain" and "legible," a narrow definition relating to grammar, presentation, and accessibility, rather than likely understanding or comprehension. Readability frameworks have been shown repeatedly to be poor indicators of whether a communication will be understood. The work of Professor Richard Hyde at the University of Nottingham has specifically demonstrated this gap between readability scores and actual comprehension outcomes.

Despite this, the FCA's Consumer Duty guidance references readability as one component of the Consumer Understanding Outcome, an approach Amplifi's research shows is materially insufficient for compliance purposes. The FCA Handbook (CONC 3.3.2) requires that communications use "plain and intelligible language" note: intelligible, not merely readable.

Intelligibility vs readability: a direct comparison

This table summarises the key differences between readability and intelligibility across six dimensions. It should serve as the reference point for any compliance team currently using readability scores as evidence of the Consumer Understanding Outcome.

Six drivers of complexity that readability frameworks miss

These are the factors Amplifi consistently identifies in regulated consumer communications that readability tools do not detect, and that create the greatest intelligibility risk.

The implications for AI-generated content are significant. Language models tend to produce communications that score well on surface readability while introducing conceptual complexity and structural issues that readability tools will not flag. For firms using AI to draft communications, this is an acute governance risk. See: AI-generated content and FCA compliance: what regulated firms must govern in 2026.

Why this distinction creates compliance risk

The FCA's position

Firms that rely on readability scores as evidence of the Consumer Understanding Outcome are not meeting the FCA's standard. The regulator has been explicit:

FCA: "Borrowers often struggle to understand complex legal and financial documents, leading to poor financial decisions and confusion. Readability scores alone usually overlook complexity and a user's comprehension."

The FCA has reviewed nearly 260 Consumer Duty board reports across the first two reporting cycles. A consistent finding across both cycles was that compliance teams submitted readability data as evidence of the Consumer Understanding Outcome, and the FCA consistently rejected this as insufficient. For the full picture of what good board report evidence looks like, see: How to write a Consumer Duty board report in 2026 and FCA Consumer Duty governance: the annual board report requirement.

The regulatory exposure

The use of readability as a proxy for intelligibility creates specific compliance risk across three regulatory regimes now operating simultaneously:

- FCA Consumer Duty: The Consumer Understanding Outcome requires firms to test whether their communications actually enable effective consumer decisions, not just that they are grammatically simple.

- Consumer Rights Act 2015: Terms not meeting the intelligibility standard may be unenforceable. A contractual term that a consumer cannot understand the consequences of may be deemed unfair.

- CMA enforcement: The Competition and Markets Authority has new powers to police the Consumer Rights Act and is actively scrutinising the intelligibility of terms and conditions. Fines of up to 10% of global turnover are available.

- Gambling Commission: The Commission has focused specifically on the need for more understandable terms in gambling contracts, another sector where readability-only testing leaves firms exposed.

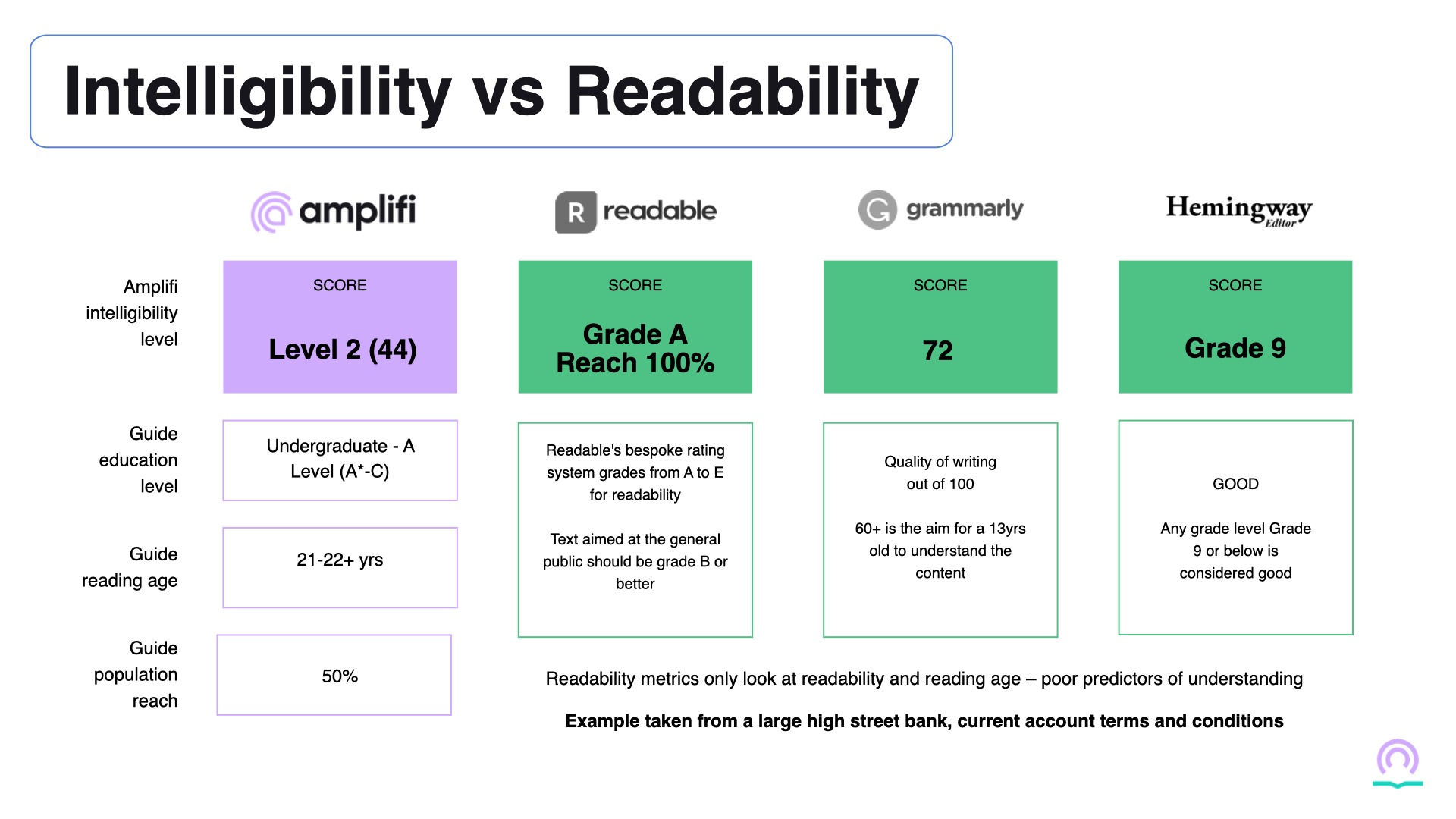

Evidence from practice: the bank T&C test

Amplifi tested the current account terms and conditions of a large UK high street bank using both Amplifi's intelligibility assessment and a range of standard readability tools. The difference in scores for the same content was striking: intelligibility assessment surfaced material risks that the readability tools did not identify. A firm relying on readability data for that document would have received a materially misleading picture of its compliance position.

KEY FINDING: A document can achieve a strong readability score and still fail the intelligibility standard. The two metrics measure different things, and only one of them is the legal requirement.

How Amplifi measures intelligibility

Amplifi is the only platform that assesses the full range of intelligibility factors, not just surface readability, against FCA Consumer Duty standards. Here is how each metric works.

The intelligibility level scale

Amplifi's Intelligibility Score (0–100) is mapped to five levels aligned to UK educational attainment and population reach. This allows firms to answer the specific Consumer Duty question: "Is this communication intelligible to our target market?" not just "Is it written in simple sentences?"

For most retail financial services communications, credit agreements, insurance policies, terms and conditions, the FCA expects firms to target Level 4 or above, ensuring the communication is accessible to the broad majority of UK consumers, including those with characteristics of vulnerability.

The Multi-Level Comprehension Framework

To ensure the purpose of a communication is fully understood, not just its surface content, Amplifi applies its Multi-Level Comprehension Framework, which distinguishes between simple recall and high-order cognitive processing.

The framework assesses a user's ability to comprehend information at various cognitive levels:

- Recall: Can the consumer identify the key facts stated?

- Interpretation: Can the consumer understand what those facts mean in their context?

- Application: Can the consumer use the information to make a decision or take action?

- Consequence: Can the consumer understand the potential risks, costs, and consequences: the foreseeability dimension required in law?

The framework has been used by the FCA in its own published research: it underpins the FCA's consultation paper CP25/17: Supporting consumers' pensions and investment decisions and the FCA research note "Reading Between the Lines: Understanding of targeted support in retail investments". It was also validated in Amplifi's research with the Solicitors Regulation Authority (SRA), which assessed and simplified regulatory guidance communications and then tested them with both consumers and legal professionals.

The SRA validation study found that simplified documents, those with higher Amplifi Intelligibility Scores, produced increased understanding outcomes across all tested groups, particularly at the higher cognitive levels needed for informed decision-making. Simplified text also improved engagement, resulted in faster reading times, and improved trust in the provider of the information.

How the Amplifi platform works

Amplifi scores every document using its Cognitive Risk Engine™ - a proprietary AI model trained on legal and regulatory communications. The engine analyses a document's architecture: structural density, sentence complexity, conceptual difficulty, and the connections between concepts. It produces an Intelligibility Score (0–100) and categorises the text into one of five levels.

Continuous, embedded testing

The score updates automatically each time a document is edited; no re-upload or manual trigger required. This removes the cadence constraints of panel-based testing, where cost, operational effort, and participant fatigue mean testing can only happen at fixed points. With Amplifi, testing is continuous and embedded into the drafting workflow.

Teams can test, improve, and retest within a single workflow, seeing the impact of each change immediately. Every draft, every edit, and every iteration is assessed against the same objective standard. This makes continuous optimisation practical across a full document portfolio - something panel-based approaches cannot sustain.

The audit trail

Every assessment is retained and time-stamped, creating a defensible compliance record. When the FCA asks how a firm satisfied itself that its communications met the Consumer Understanding Outcome, an assessment record produced at the point of approval is the kind of answer that demonstrates genuine governance, not aspiration. This is especially critical for firms using LLMs or AI tools to draft communications, where the risk of producing fluent but unintelligible content is structural. For more on this, see: Why LLMs cannot substitute for a compliance-grade intelligibility assessment.

Conclusion

Readability and intelligibility are not the same thing. Readability measures whether text is easy to process. Intelligibility measures whether the target reader can understand the content, contextualise it, act on it, and foresee its consequences. The first has no clear legal definition. The second is what the FCA Consumer Duty, the Consumer Rights Act 2015, and CJEU case law require.

Firms that rely on Flesch-Kincaid scores or similar metrics as evidence of the Consumer Understanding Outcome are not meeting the regulatory standard, and are creating a compliance gap that readability tools are structurally incapable of detecting.

Amplifi's Cognitive Risk Engine™ is the only platform that assesses intelligibility in full - across all six drivers of complexity, mapped to UK population reach, and producing a reproducible, auditable evidence trail. To see how it applies to your communications portfolio, visit amplified.global/product or contact the team.

Further reading

What is the FCA Consumer Duty? A plain-English guide

AI-generated content and FCA compliance: what regulated firms must govern in 2026

How to write a Consumer Duty board report in 2026

FCA Consumer Duty governance: the annual board report requirement

Amplifi Multi-Level Comprehension Framework (PDF)

FCA CP25/17: Supporting consumers' pensions and investment decisions

FCA research note: Reading Between the Lines

SRA and Amplifi: beyond readability: what the trial taught us about legal clarity

Why LLMs cannot substitute for a compliance-grade intelligibility assessment

About Amplifi

Amplifi (Amplified Global Ltd) is a UK-based AI software company whose Cognitive Risk Engine™ helps FCA-regulated firms assess, simplify, and evidence the intelligibility of customer communications for Consumer Duty compliance. ISO 27001 certified, FSQS registered, FCA Sandbox tested, and listed on the FCA AI Marketplace 2025. The Amplifi Comprehension Framework was cited in FCA Consultation Paper CP25/17. Visit amplified.global.

Explore more articles