FCA Consumer Duty & Consumer Understanding

Embedding intelligibility at the heart of outcomes-based regulation.

The FCA Consumer Duty represents a step change in UK financial regulation, placing consumer understanding and fair outcomes at the centre of regulatory expectations. Intelligibility is no longer implicit it is a measurable requirement across communications, products, and contractual terms.

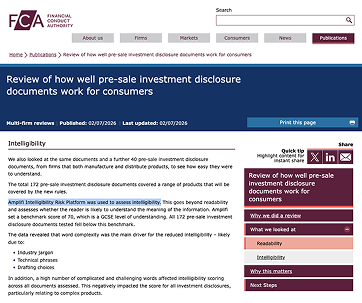

The FCA use Amplifi to benchmark the investment market.

The FCA used Amplifi to test 172 pre-sale investment disclosure documents for intelligibility.

The results set a sector benchmark ahead of new CCI rules in 2027. This signals what good and bad disclosure looks like. Expect more studies across credit cards, debt, and legal agreements.

Collaborating to pioneer transformational

AI in Financial Services and beyond

Collaboration with the FCA since 2019. Supported by the FCA Innovation Service and featured in the FCA AI Marketplace. Our consumer comprehension research has informed policy discussions and internal regulatory research.

Amplifi Research

Pioneering research informing policy change

Amplifi Comprehension framework used to inform consultations for supporting consumers pension and investment decisions and the research in understanding targeted support for retail investment

.png)

FCA Consumer Duty: Ensuring Consumer Understanding and Fair Outcomes

↓ 35%

Carbon Emissions in 18 months

What the FCA Consumer Duty Requires

The Consumer Duty introduces a higher standard of conduct for firms, requiring them to act to deliver good outcomes for retail customers. Central to this is the requirement that consumers can understand the information they are given and make effective, informed decisions.

The Duty applies across the lifecycle of financial products and services, from design and pricing to communications and ongoing support. Firms must demonstrate that consumer understanding is actively considered, tested, and monitored.

FCA Principle 12: A firm must act to deliver good outcomes for retail customers.

FCA Principle 12: A firm must act to deliver good outcomes for retail customers.

↓ 35%

Carbon Emissions in 18 months

Understanding Is Not Assumed - It Must Be Evidenced

Under the Consumer Duty, consumer understanding is a defined outcome, not a by-product of disclosure. The FCA expects firms to consider how information is presented, whether it is likely to be understood by the intended audience, and how comprehension can be evidenced.

This shifts regulatory focus from volume of information to clarity, relevance, and usability — particularly for complex products and contractual terms.

- Clear, timely, and relevant communications

- Avoidance of foreseeable harm caused by complexity

- Testing communications for comprehension, not just accuracy

+20%

Energy reduction data operations

Applying an Intelligibility Lens to Consumer Duty

An intelligibility-led approach transforms Consumer Duty compliance from a subjective guessing game into validated evidence of good consumer outcomes. By quantitatively assessing whether your language, structure, and presentation enable genuine understanding, Amplifi ensures you are not just disclosing information, but actively empowering customers and protecting your firm from enforcement risk.

+34%

Increase in bio diversity

Why Intelligibility Matters for Supervision and Outcomes

An intelligibility-focused approach supports the FCA’s supervisory objectives by enabling clearer assessment of how firms meet Consumer Duty expectations. It strengthens the link between regulatory intent, firm behaviour, and consumer outcomes.

By focusing on comprehension rather than disclosure alone, regulators and firms alike can better identify risk, prevent harm, and support fair market functioning.

+62%

Carbon Emissions in 18 months

Consumer Duty as a Foundation for Trust

The FCA Consumer Duty establishes intelligibility as a foundation for fair treatment and consumer trust. As outcomes-based regulation continues to evolve, the ability to assess and evidence consumer understanding will remain central to effective supervision and market confidence.

Our Journey

2019

Joined the FCA Innovation Hub

Received FCA innovation support to refine our thinking on intelligibility and consumer understanding

.png)

Our Journey

2020-21

FCA Digital Sandbox

Tested early AI language models and tooling to address emerging regulatory challenges

Our Journey

2022

Mixed Messages Report

Launched Mix Messages report with StepChange Debt Charity at the FCA event, with a keynote speech from Sheldon Mills (FCA Exec Director)

Our Journey

2023

FCA Regulatory Sandbox

Live testing on consumer understanding - disclosure notices, PCI and default notice

Our Journey

2024

Solicitors Regulation Authority (SRA)

Amplifi collaborated with the SRA in testing intelligibility and improving understanding of regulation / guidance

Our Journey

2024

Ongoing FCA Innovation Support

Amplifi received ongoing innovation support from the FCA to develop layered digital credit contracts

Our Journey

2025

FCA AI Spotlight

Amplifi was accepted onto the FCA’s AI marketplace. A shop window for leading AI companies operating within financial services

Our Journey

2025

Our research referenced by the FCA

Amplifi Comprehension Framework used in FCA research (CP25/17), and consultation for targeted support

Our Journey

2025

FCA Digital Sandbox

Developing AI models to identify risk in Maths, numbers, tables, charts and cognitive load.

Our Journey

2025

FCA / MAS AI Round Table

Amplifi invited by FCA AI lab to showcase our Intelligibility Risk Platform to the Monetary Authority of Singapore (MAS).

Our Journey

2025

HMT Consumer Credit Act Consultation

Amplifi regulatory sandbox work and evidence on consumer understanding for Pre Credit Info (PCI) and Default notice used and mentioned in the consultation.

Intelligibility is not an enhancement to

regulation - it is how regulation works

in practice.

Amplifi & The FCA

Over a six-year period, Amplifi Global have received a range of Innovation Service support tailored to changing needs across their full innovation lifecycle.

1. Amplifi received support via Innovation Pathway, including an informal steer on precontractual disclosures and adequateexplanation requirements in CONC 4.2 and CONC 7.3.

2. Amplifi concept development in the Digital Sandbox, followed by live test with a regulated credit provider in the Regulatory Sandbox, to ensure alignment with Consumer Duty principles.

3. In collaboration with Universities, the firm have conducted research into consumer comprehension, which has informed FCA policy discussions and contributed to internal research.

2. Amplifi concept development in the Digital Sandbox, followed by live test with a regulated credit provider in the Regulatory Sandbox, to ensure alignment with Consumer Duty principles.

3. In collaboration with Universities, the firm have conducted research into consumer comprehension, which has informed FCA policy discussions and contributed to internal research.

Significant progress in product development with FCA guidance

The tool's effectiveness was validated using Regulatory Sandbox and supporting research

Results will support engagement with lenders aiming to meet Consumer Duty standards

Explore Regulatory blogs

The Knowledge Hub is Amplifi’s home for blogs on research, insights, and tools that put consumer understanding at the centre of compliance, finance, law, and AI.

Your AI-Powered Workflow.

© 2026 All rights reserved