Summary

What this article covers: what the Consumer Duty is, the four outcomes, what firms must evidence, the board report requirement, and how intelligibility testing meets the standard readability scores cannot.

The FCA Consumer Duty represents a fundamental shift in UK financial regulation; from a focus on process and legal disclosure to a mandatory, evidence-based focus on achieving positive consumer outcomes. Introduced in July 2023, it requires all FCA-regulated firms to act to deliver good outcomes for retail customers across four areas: products and services, price and value, consumer support, and consumer understanding.

Of these four outcomes, consumer understanding is the one most directly tied to the clarity of written communications, and the area where most firms remain most exposed. This article explains the Duty's requirements in full, with particular focus on what evidencing consumer understanding actually requires in 2026.

Related reading: Intelligibility vs readability: what the FCA actually requires | AI-generated content and FCA compliance | How to write a Consumer Duty board report in 2026

The aims of the Consumer Duty

The Consumer Duty is an outcomes-focused regulatory framework that compels firms to put retail consumers' interests at the centre of their business models, not just in policy documents, but in demonstrated practice. It moves well beyond the previous standard of 'treating customers fairly' and mandates that firms actively prevent foreseeable harm and equip consumers to make effective, informed decisions.

The FCA published its final rules and guidance in Policy Statement PS22/9 in July 2022. The core aims are:

- Higher, clearer standards: A universally high level of consumer protection across all financial services sectors.

- Real-world consumer outcomes: Firms must actively prevent foreseeable harm and equip consumers to make effective, informed financial decisions.

- Public trust: A consumer-centric financial culture where firms compete on genuine value and service quality, not consumer confusion or inertia.

Obligations placed on firms

Regulatory obligations

Principle 12, The Consumer Principle: The overarching rule requires firms to "act to deliver good outcomes for retail customers." It replaces Principles 6 and 7 for retail business and sets the standard against which all Consumer Duty compliance is measured. See the FCA Handbook PRIN for the full text.

The Cross-Cutting Rules require firms to:

- Act in good faith toward retail customers

- Avoid causing foreseeable harm to retail customers

- Enable and support retail customers to pursue their financial objectives

The shift in burden of proof

Practically, the Duty shifts the burden of proof onto the firm. It is no longer sufficient to argue that a process is not intentionally unfair. Firms must actively demonstrate, with evidence, that their customers are achieving good outcomes. Assertions are not evidence. MI dashboards alone are not evidence. The FCA expects firms to test their communications, retain the results, and present them when asked.

KEY PRINCIPLE: The Consumer Duty does not ask firms to prove they have a process. It asks them to prove that the process is working; that consumers are actually understanding, benefiting, and making effective decisions as a result of the firm's communications and products.

The four Consumer Duty outcomes

The four outcomes are the operational heart of the Consumer Duty. Firms must design, execute, and review their business against each one.

1. Products and services

All products and services targeted at retail consumers must be fit for purpose and designed to meet the specific needs, characteristics, and objectives of a defined target market. Firms must ensure products are distributed appropriately to avoid mis-selling to consumers outside that target group. This outcome requires product governance frameworks that document the intended target market and evidence that distribution channels reach it accurately.

2. Price and value

Firms must ensure a reasonable relationship exists between the price a consumer pays and the overall benefit they receive. The FCA is actively targeting excessive hidden fees, loyalty penalties - where existing customers are charged substantially more than new customers without justification - and low-value add-ons. Price and value assessments must be documented and revisited regularly, with evidence that the firm has considered the full picture of benefits received.

3. Consumer understanding

This is the outcome most directly relevant to written communications, and the one where most firms remain most exposed. Communications must do more than meet the legal minimum of being "clear, fair, and not misleading." They must actively support and enable consumers to make informed choices. Information must be provided at the right time, in the right format, and in a way the target audience can genuinely comprehend.

The FCA has been explicit that readability scores are not a sufficient proxy for consumer understanding. The distinction between readability and intelligibility is central to meeting this outcome - see our dedicated article: Intelligibility vs readability: what regulated firms need to know.

"Borrowers often struggle to understand complex legal and financial documents, leading to poor financial decisions and confusion. Readability scores alone usually overlook complexity and a user's comprehension." FCA

4. Consumer support

Firms must provide a level of support that meets consumers' needs throughout the entire product lifecycle. Buying, switching, amending, and cancelling a product must be equally seamless. The FCA expects firms to monitor support outcomes actively, e.g. call abandonment rates, resolution times, escalation frequencies, and to provide appropriate access for customers with characteristics of vulnerability, including those who are digitally excluded.

Testing, simplification, and monitoring

The FCA expects firms to move past superficial checklists and embrace continuous operational refinement through testing, simplification, and outcome-driven monitoring. The following framework covers what each stage requires.

Testing requirements

For a detailed explanation of why readability frameworks fail the intelligibility test, including the legal basis from CJEU case law and the Consumer Rights Act 2015, see: Defining intelligibility vs readability. For firms using AI tools to draft communications, the governance implications are covered in: AI-generated content and FCA compliance: what regulated firms must govern in 2026.

Simplification and tailoring

Simplification means removing needless complexity from communications, not just shortening them, but reducing cognitive load. Tailoring means ensuring communications accommodate varied consumer needs, particularly for vulnerable customers. These are not design preferences; they are regulatory requirements. The FCA expects firms to evidence that they have identified and addressed communications that create unnecessary complexity for their target audience.

Monitoring outcomes

Firms must shift from process-driven metrics to outcome-driven metrics. Confirming that 10,000 renewal letters were sent is not evidence of good outcomes. Evidence requires asking whether those letters resulted in customers acting in their own best interests, and having data to support the answer.

Robust Management Information (MI) must draw on multiple data sources: complaint root-cause analysis, customer drop-off rates during digital journeys, FOS data, comprehension testing results, and direct customer research. Boards must receive this data in a form that allows genuine challenge, not just confirmation.

Governance and the annual board report requirement

The FCA places ultimate accountability for Consumer Duty compliance at board level. The board report is the primary document the regulator examines in supervisory dialogue.

At least once a year, a firm's governing body must formally review and approve an extensive assessment report detailing whether the firm is delivering good outcomes across all four outcomes. The next deadline is 31 July 2026.

The report must cover:

- Outcomes assessment: Granular MI across all four pillars proving customers are achieving good outcomes. Not assertions, but data.

- Gap and risk identification: Transparent documentation of areas where the firm fell short or poor outcomes were detected, including root cause analysis.

- Remedial actions: Time-bound action plans with clear ownership and measurable effectiveness criteria for every identified gap.

- Strategic alignment: Formal board certification that the firm's future business strategy is consistent with its Consumer Duty obligations under Principle 12.

The FCA has reviewed nearly 260 Consumer Duty board reports across the first two cycles and published detailed findings in February 2026. For a full guide to what the 2026 report must contain, including the specific weaknesses the FCA found in previous cycles, see: How to write a Consumer Duty board report in 2026. For the governance requirements specifically, see: FCA Consumer Duty governance: the annual board report requirement.

What the FCA found lacking in board reports

The FCA's review of first- and second-cycle board reports identified consistent weaknesses. Firms that produced poor reports shared these characteristics:

- Readability as a proxy for understanding: Compliance teams reported Flesch-Kincaid scores or similar metrics as evidence of the Consumer Understanding Outcome. The FCA has explicitly rejected this approach.

- Aggregated MI: Data was presented at a level too broad to identify specific harms or differentiate outcomes for vulnerable customer groups.

- Absent board challenge: Reports were approved without substantive discussion. Board minutes showed no evidence that directors had questioned the data or challenged compliance conclusions.

- No intelligent action on vulnerable customers: Firms failed to demonstrate separate evidence that vulnerable customers were achieving outcomes equivalent to the general population.

KEY POINT: The era of tick-box compliance is over. The FCA penalises cookie-cutter and purely narrative reports. Boards are expected to receive high-quality, segmented, intelligibility-focused evidence, and to demonstrate they have challenged it.

How Amplifi aligns to the Consumer Duty

Amplifi's methodology was developed with direct and ongoing FCA support. Its regulatory credibility is not a marketing claim, it is a documented, tested track record.

Regulatory validation

Amplifi's first FCA Sandbox test provided a robust evidence base for CCA reform currently under review by HM Treasury and the FCA. By testing the impact of simplifying Pre-Contract Credit Information (PCI) and Default Notices at the FCA's request Amplifi demonstrated that plain and intelligible language is a fundamental driver of consumer agency.

The Amplifi Comprehension Framework was cited in FCA Consultation Paper CP25/17 on targeted support. The HM Treasury Policy Statement on CCA Reform (15 May) directly references Amplifi's research on page 39. These are not indirect endorsements, they are direct citations of Amplifi's methodology in live regulatory consultations.

Amplifi is ISO 27001 certified, FSQS registered, and listed on the FCA AI Marketplace 2025.

How Amplifi addresses each Consumer Duty obligation

How Amplifi works

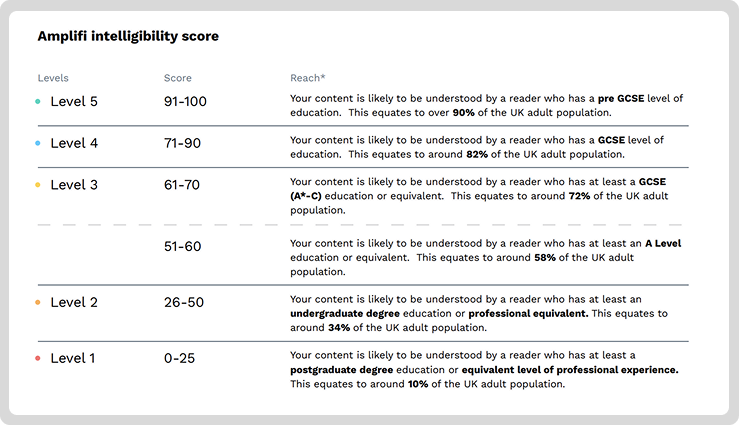

Amplifi scores every document using its proprietary Cognitive Risk Engine™. The score measures how intelligible a communication is likely to be for a given reader group - going beyond standard readability metrics to assess conceptual complexity, ambiguity, and genuine comprehension risk. It is expressed as a numeric score mapped to a five-level intelligibility scale, where Level 1 represents the highest risk and Level 5 represents the lowest.

Continuous, embedded testing

Intelligibility scores update automatically each time a document is edited so there's no need to re-upload or manually trigger a new assessment. This removes the cadence constraints of panel-based testing, where cost, operational effort, and participant fatigue mean testing can only happen infrequently. With Amplifi, testing is continuous and embedded into the drafting workflow itself.

The platform supports iterative testing across multiple document versions. Teams can test, improve, and retest within a single workflow, compressing what would otherwise be a lengthy review and revision cycle. This makes continuous optimisation practical at scale across a full document portfolio. For firms generating content using AI tools, Amplifi assesses AI-generated communications against the same standard as human-authored content. See: AI-generated content and FCA compliance.

Intelligibility over readability

While readability scores create false confidence, Amplifi's methodology assesses intelligibility - the fundamental requirement in law and regulation to ensure consumers can read, understand, and apply information to make an informed decision. This distinction is grounded in the Consumer Rights Act 2015, CJEU case law on intelligibility and foreseeability, and the FCA's own Consumer Duty guidance. For the full legal basis, see: Defining intelligibility vs readability.

The Consumer Duty timeline

Phase 1: open products and services

- July 2022: FCA published the final rules and guidance (PS22/9)

- October 2022: Firms' boards agreed implementation plans

- April 2023: Manufacturers completed reviews for existing open products and shared outcomes with distributors

- July 2023: Implementation deadline -all new and existing products or services open to sale or renewal

Phase 2: closed products and services

- July 2024: Implementation deadline for closed products and services (legacy contracts no longer marketed to retail customers)

Recent updates and upcoming deadlines

- February 2025: FCA provided greater governance flexibility, removing the explicit requirement for firms to appoint a Consumer Duty Board Champion

- Ongoing 2025/26: FCA in its impact phase - cross-cutting reviews of consumer understanding, customer journey design, and outcomes monitoring underway

- 31 July 2026: Deadline for firms to complete their next cycle of annual Consumer Duty board reports

Conclusion

The Consumer Duty has fundamentally changed what regulated firms must prove, and how. The shift from process compliance to outcome evidence is permanent. The four outcomes demand firms test, monitor, and report against real consumer behaviours, not theoretical standards. And of those four outcomes, consumer understanding is the one most directly tied to the quality of written communications, and the one where firms' current evidence — often relying on readability scores — falls most clearly short of what the FCA expects.

Amplifi was built specifically to close that gap. Its Cognitive Risk Engine™ delivers the intelligibility evidence the Consumer Understanding Outcome requires: objective, reproducible, and in a format designed for board-level consumption.

To see how the platform applies to your communications portfolio, visit amplified.global/product or contact the team.

Further reading

Intelligibility vs readability: what the FCA actually requires

AI-generated content and FCA compliance: what regulated firms must govern in 2026

How to write a Consumer Duty board report in 2026

FCA Consumer Duty governance: the annual board report requirement

FCA Policy Statement PS22/9: Consumer Duty final rules

Amplifi Multi-Level Comprehension Framework (PDF)

About Amplifi

Amplifi (Amplified Global Ltd) is a UK-based AI software company whose Cognitive Risk Engine™ helps FCA-regulated firms assess, simplify, and evidence the intelligibility of customer communications for Consumer Duty compliance. ISO 27001 certified, FSQS registered, FCA Sandbox tested, and listed on the FCA AI Marketplace 2025. The Amplifi Comprehension Framework was cited in FCA Consultation Paper CP25/17. Visit amplified.global.

Explore more articles