FCA Consumer Duty: Governance & The Annual Board Report Requirement

FCA Consumer Duty: Governance & The Annual Board Report Requirement

The FCA firmly places ultimate accountability for the Consumer Duty at the board level. The Duty is not an isolated compliance desk exercise. It is a core governance responsibility.

The Annual Board Report Mandate

At least once a year, a firm’s governing body (the Board) must formally review and approve an extensive assessment report detailing whether the firm is delivering good outcomes for its customers.

The board report must cover several crucial elements:

- Outcomes Assessment: A granular review of the monitoring data and MI across all four pillars to prove that customers are getting good outcomes.

- Gap and Risk Identification: Transparent documentation of any areas where the firm fell short, where poor outcomes were detected (especially regarding vulnerable groups), and a clear analysis of the root causes.

- Remedial Actions: An explicit, time-bound action log outlining exactly how the firm is fixing identified gaps, who owns the risk, and how the effectiveness of those fixes will be measured.

- Strategic Alignment: The Board must formally certify that they are satisfied the firm is complying with the Duty, and that the firm’s future business strategy and growth plans are entirely consistent with its regulatory obligations.

The FCA regularly requests and reviews these internal board reports to assess a firm’s compliance maturity. The regulator explicitly penalises cookie-cutter or purely narrative reports, demanding instead heavily data-backed, self-critical, and proactive evidence of good consumer outcomes.

As the deadline for the next cycle of Consumer Duty board reports approaches on 31 July 2026, the era of tick-box compliance is firmly over.

For firms regulated by the Financial Conduct Authority (FCA), this report is not merely a mandatory attestation, it’s a critical piece of internal governance and a formal review of how the Duty is being embedded across the business.

The FCA has been clear: ultimate accountability for consumer outcomes sits with boards and senior management. Relying on high-level percentages or vague assertions will no longer suffice.

1) Focus on High Quality Testing Beyond Readability

It is critical Boards can distinguish between readability and intelligibility in the senior-level Management Information they receive. The FCA has signalled that they won’t trust standard readability scores as a proxy for understanding.

“Borrowers often struggle to understand complex legal and financial documents, leading to poor financial decisions and confusion. Readability scores alone usually overlook complexity and a user's comprehension….” (FCA).

Relying on readability data alone leaves significant residual risk, as it fails to measure whether a consumer can truly understand and use the information.

Objective intelligibility and comprehension testing is the new standard the FCA expects.

If a Board report relies on readability, is the report compliant?

Firms should have tested all their communications and yet we know they haven’t. The latest update from FCA confirmed as much.

Will your firm be able to provide evidence across all communication asked for by the FCA?

2) Learning from the Past: Good vs. Bad Practice

Last year’s reporting cycle provided a wealth of insight into the FCA’s expectations. In its recent review of board reports, the regulator identified distinct patterns of good practice:

- Segmented Outcome Monitoring: Stronger reports translated high-level Management Information (MI) into real-world indicators, testing comms, and analysing outcomes for specific customer groups and individual products.

- Proactive Testing: Firms that performed well did not just rely on complaints data. They actively tested communications using validated tools and effective methods, and using tools like comprehension checks to verify understanding.

- Actionable Insights: Good reports clearly documented what was discovered, why changes were made, and the measurable impact of those changes.

3) The Shift to Richer Data and MI

The FCA is increasingly focused on the quality of MI. Boards are now expected to push beyond simple data points and seek insights that provide a sufficient basis for determining if consumers are truly receiving good outcomes. This shift requires richer data, including information that goes beyond the absence of poor indicators to demonstrate why firms are confident their consumers will achieve good outcomes.

This is particularly relevant for the Consumer Understanding Outcome. Firms must now evidence how they test communications and how they respond when consumer behaviours indicate misunderstanding or friction. Without high-quality data, boards cannot satisfy themselves that the firm is compliant or identify emerging risks.

4) The Requirement for Board Challenge

A vital element of the 2026 report is demonstrating that the board has not been a passive recipient of information. The FCA expects to see evidence of active challenges driven by quality internal data. They must show that they have questioned whether monitoring is adequate, interrogating deteriorating metrics, and directing corrective actions.

Board minutes should reflect these discussions, as the regulator will scrutinise firms and underlying evidence to ensure the board is taking its obligations seriously. Firms must be prepared to show not just that a process exists, but that the process has been improved through board-level oversight.

How does Amplified Global align to the Consumer Duty?

Amplified Global’s first FCA Sandbox test has provided a robust evidence base for the Consumer Credit Act (CCA) reform currently under review by HM Treasury and the FCA. By testing the impact of simplifying Pre-Contract Credit Information (PCI) and Default Notices (at the request of the FCA), we demonstrated that "plain and intelligible language" is a fundamental driver of consumer agency.

Our research has directly informed the FCA’s and HM Treasury's thinking on the future of consumer credit. In the CCA Reform Phase 1 Consultation. The consultation’s focus on layering, navigability, and well-timed communication mirrors the exact techniques we refined during our Sandbox trial. Specifically, the move away from the "presumption that a ‘one size fits all’ approach can be effective" is supported by our evidence. The recent HM Treasury Policy Statement on Reform of the CCA on 15 May directly references our research (page 39).

Amplified Global’s methodology, developed with direct and ongoing support from the FCA, is purpose-built to align with the Duty by providing firms with the tools to objectively measure and prove these outcomes. The alignment is evidenced through the following pillars, which help our clients to achieve and demonstrate their compliance with the testing, tailoring and monitoring requirements:

Evidence-Based Compliance: Our platform provides a science-backed, data-driven audit trail that firms use to demonstrate to the FCA that they are actively testing and improving consumer understanding.

Intelligibility Over Readability: While readability scores often create false confidence, our methodology assesses intelligibility, the fundamental requirement in law and regulation to ensure that consumers can read, understand, and then apply information to make an informed decision.

Consumer-First Assessment: Our methodology specifically identifies where cognitive load and structural density harm understanding for particular cohorts, including vulnerable consumers, such as those with lower financial literacy, low income, or those without English as a first language. This allows firms to test and tailor communications to meet the diverse needs of all customers.

Validated Innovation: Through the research in the FCA Sandbox, and with SRA, we have validated that simplified documents with a higher Amplifi Intelligibility Score result in better understanding outcomes for all consumer groups.

Beyond the existing requirements of the Consumer Duty, we already align with the incoming move by the FCA to loosen prescriptive regulation (e.g. changing investment and credit disclosures), and to place greater emphasis on firms to evidence positive outcomes and provide richer data.

We are also aligned to help clients test against the requirements of the CMA’s new Draft Guidance on Unfair Terms and the increased guidance around Transparency and Fairness. Fundamentally, from day 1 we have ensured we align ourselves directly to the requirements of the FCA Consumer Duty regulation, CMA requirements, and the underpinning law around Intelligibility and Foreseeability.

How does Amplifi work?

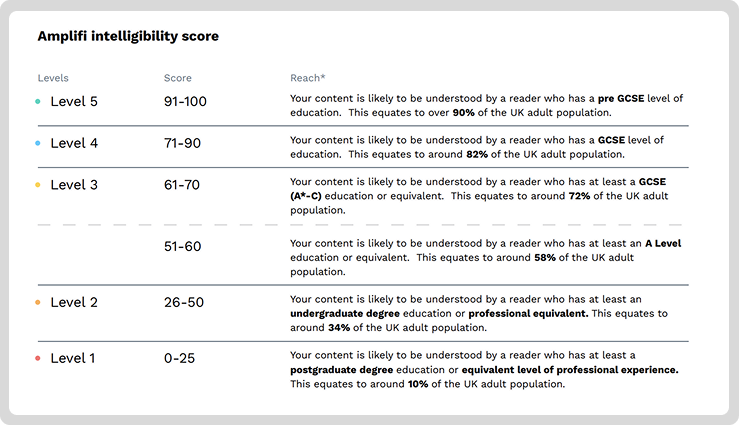

Amplifi scores every document using its proprietary Cognitive Risk Engine. The score measures how intelligible a communication is likely to be for a given reader group, going beyond standard readability metrics to assess conceptual complexity, ambiguity, and genuine comprehension risk. It is expressed as a numeric score mapped to a five-level intelligibility scale, where Level 1 represents the highest risk and Level 5 represents the lowest.

Users can see intelligibility scores across their entire portfolio and prioritise documents with the highest consumer understanding risk. The score then updates automatically each time a document is edited. There is no need to re-upload or manually trigger a new assessment. Amplifi is designed to support iterative testing across multiple versions of the same document. Teams can test, improve, and retest within a single workflow, seeing the impact of each change immediately and adjusting accordingly. This removes the cadence constraints that limit panel-based testing, where cost, operational effort, and participant fatigue mean testing can only happen infrequently and at fixed points in the drafting process. With Amplifi, testing is continuous and embedded into the drafting process itself.

Every draft, every edit, and every iteration is assessed automatically against the same objective standard (intelligibility). Teams can see the impact of a change immediately and adjust accordingly, compressing what would otherwise be a lengthy review and revision cycle into a single workflow. This makes rapid iteration practical at scale, supporting the kind of ongoing optimisation that panel-based approaches cannot sustain across a full document portfolio.

Intelligibility and readability are not the same thing. This guide explains the legal definition of intelligibility, why readability scores like Flesch-Kincaid fall short, and what the FCA's Consumer Duty actually requires.

Explore more articles