The Crypto Rejection Risk: Why Your T&Cs Could Kill Your FCA Application

.jpg)

The Approaching Regulatory Wall

The unregulated UK cryptoasset sector is officially facing a cliff edge. For years, crypto firms operated on the fringes of traditional financial regulation, but the introduction of the Financial Services and Markets Act (Cryptoassets) Regulations 2026 has firmly brought these activities within the UK regulatory perimeter.

By the time the full regime goes live in 2027, the Financial Conduct Authority’s (FCA) uncompromising Consumer Duty rules will fully apply.

Right now, we are in a critical phase of preparation and application. The Pre-Application Service (PASS) went live on 11 May, and as of this month, firms can officially request pre-application meetings to discuss their business models and risk profiles. The formal regulatory authorisation gateway then opens on 30 September 2026. But here is the uncomfortable truth that many crypto leadership teams are ignoring: the FCA has explicitly warned that "poor quality" or late applications face immediate rejection.

To pass through the gateway, firms must align their operations with the Consumer Duty’s strict standards of communication clarity from the very outset. If you think you can coast by simply tweaking a few legal definitions in your terms and conditions, you are in for a shock.

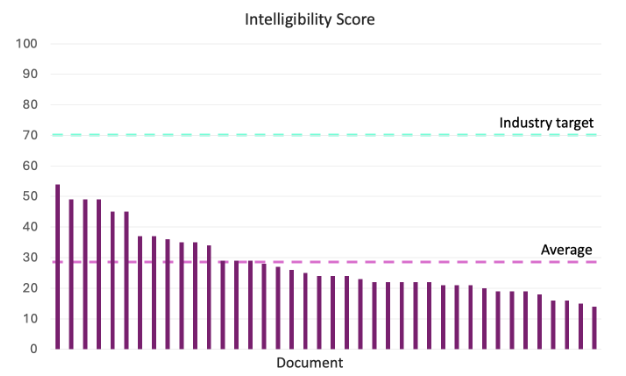

At Amplified Global, we recently conducted our 2026 Crypto Market Assessment, using our Intelligibility Risk EngineTM to analyse customer-facing documents across the sector. The results are deeply alarming for compliance teams and senior leadership alike. Across all the documents tested, not a single one reached the financial services compliance target score, which is 70 for most documents.

In fact, the average crypto intelligibility score was an abysmal 29.

To put that into perspective, the average crypto customer agreements are too long, highly complex, university-grade documents, but aimed at a mass-market audience. They average over 14,500 words and are fully understandable to just a third of the UK adult population - and that is assuming they actually sit down to read them. Over half of the industry's communications collapse into Level 1, our highest-risk category, meaning they are intelligible to a mere 10% of UK adults.

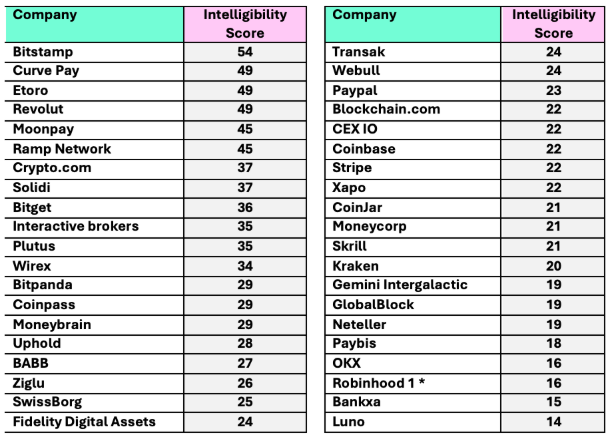

Full results of the brands we tested:

The Least Intelligible Sector (and how to fix it)

When we compare cryptoassets to other heavily regulated sectors, the data shows that crypto is an outlier of unnecessary complexity. Even notoriously dense documents like pension policies (scoring an average of 41), legal client care letters (44), and credit card agreements (52) vastly outperform cryptoasset terms, which sit at the absolute bottom of our database at an average of just 29 out of a possible 100.

Some in senior leadership might look at market leaders for reassurance, but the benchmarks tell a story of systemic failure across the board. While Bitstamp’s Key Information Document led the pack with a score of 54, its parent brand Robinhood saw its core Account Terms and Conditions plummet to a score of just 16.

At the absolute bottom was Luno, achieving an intelligibility score of 14, a level of postgraduate complexity that leaves 90% of consumers unable to understand them.

This is where the real jeopardy lies for senior leadership. Under the new regime, the FCA establishes strict liability for misleading statements or material omissions in crypto disclosures.

Under the Consumer Rights Act and the recent Digital Markets Competition and Consumers Act, the Competition & Markets Authority (CMA) has powerful new mechanisms to directly intervene and fine operators up to 10% of their annual turnover if contracts fail the test of intelligibility.

If your terms require a master’s degree to comprehend, you aren't just facing an FCA application rejection. You are walking into an operational and financial landmine.

Our statistical analysis shows that the primary driver of this failure isn't just technical jargon, it's the structural architecture of how these terms are constructed. Long, rambling sentences with nested clauses break down entirely, creating systematic consumer confusion. To fix this, firms must move away from an ‘all-in-one’ legal drafting style, enforce hard sentence length caps of 15–20 words, and leverage progressive disclosure to layer complex technical definitions away from core consumer rights.

The regulatory clock is ticking down to September 30. The FCA will not accept subjective assurances or standard readability scores as proof of compliance. They require empirical, data-driven evidence that your customers can understand your terms in practice.

This is exactly why we built Amplifi.

Developed with direct FCA innovation support since 2019 and validated in the FCA’s own Regulatory Sandbox, Amplifi uses AI and advanced linguistic models to score, diagnose, and streamline your critical communications.

Don't let poor document structure turn your PASS application into an immediate rejection. Reach out to me at ewan@amplified.global today to see your platform’s scores and protect your business before the gateway closes.

Explore more articles