FCA Consumer Duty Focus: FCA doubles down on clarity

Why credit cards are suddenly in the firing line

The Financial Conduct Authority’s recent note narrowing its Consumer Duty focus areas passed many by, yet its consequences could be far reaching.

The note reminds the market that the Duty is central to the FCA's 2025–26 agenda. The regulator has chosen specific areas and topics to focus on. This includes giving consumers clear, usable information, and a targeted look at consumer credit products. And the focus has now turned to credit cards.

This isn’t happening in isolation. The Duty sits central to the FCA’s wider five-year strategy, which was published earlier in the year. As part of that strategy, the regulator plans to “deepen trust, rebalance risk, support growth and improve lives.” That strategy makes clear the Consumer Duty isn’t a tickbox exercise. It is part of the FCA’s long term plan to hold markets to higher standards over the next five years, and underpins the ongoing CCA and BNPL reforms.

So what should you be looking out for?

- The FCA’s increasing emphasis on consumer understanding

- A big focus on credit-cards

You may want to consider two possible longer-term impacts:

- More aggressive enforcement

- Potential for future legal challenges

Consumer clarity is a priority

It is clear from the FCA’s focus areas that they expect firms to give consumers information that they can use to make better decisions. Too many documents remain legally robust but hard to understand. This is despite the Duty being in place for two years now. Firms have moved too little, and too slowly.

Under the outcome-focused regime, firms need evidence that customers actually understand product features, costs and risk. We expect the FCA to lean further into behavioural testing. They will want more data on how consumers use information, and how that creates real changes to consumer journeys. This is the focus of our new product in development, enabling clients to gain insights in situ as part of the consumer journey.

From a practical perspective, this means more than cosmetic edits to copy. It means firms must show how testing has resulted in better comms and products.

Credit cards are the new hot spot

Most strikingly, the FCA has singled out consumer credit — and credit cards in particular — as an area of concern. That’s significant. It links the Duty’s expectations about clear communications directly to a product where complex pricing, fees and contract mechanics have long frustrated consumers.

The FCA’s focus means credit-card firms can expect deeper thematic work. This could lead to potentially enforcement if communications and terms fall short.

This comes in the shadow of the motor finance case that dominated the headlines this summer. The decision is costing the industry billions and has already created a wave of media and activity by consumers and CMCs. It shows how quickly a legal challenge can lead to mass compensation claims.

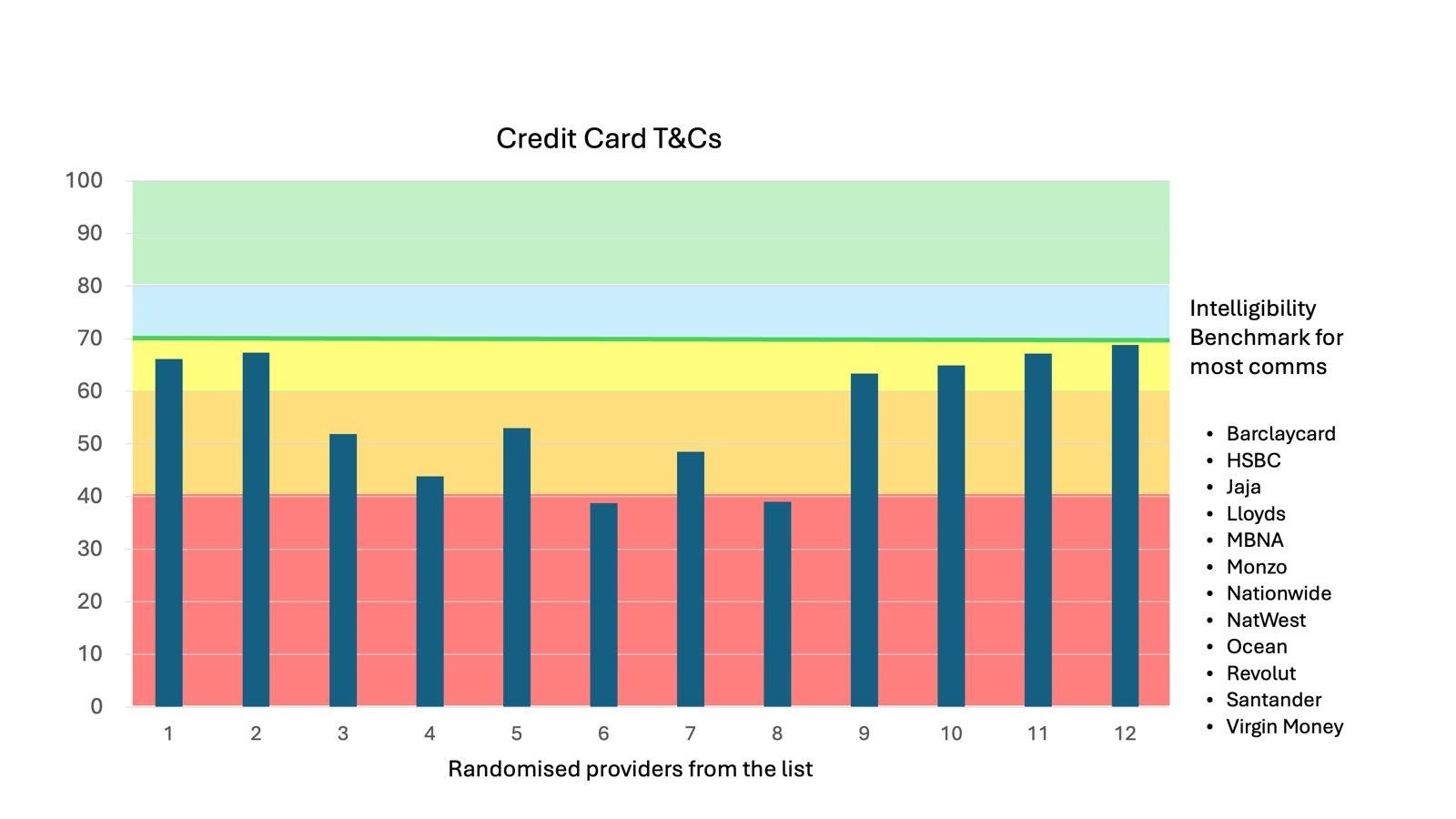

When we used Amplifi to test a range of current credit card terms, we were shocked by the results. Very few terms reached what we would consider a compliant level of intelligibility. This means that a wide range of consumers (and in many cases a majority) would find them seriously challenging to understand.

Explore more articles