The Emotional Cost of Reading: How Credit Card Agreements Make People Feel

Introduction

The previous article, "The Language Trap: Why Consumers Struggle to Engage with Credit Card Agreements," showed how the specific language used in credit card agreements hinders consumer engagement. This project was a collaboration with Professor Maggie Chen and the Cardiff University research team and was funded by UKFIN+.

In this article, we look at what happens next: the emotional impact. We explore how anxiety, stress, and mistrust arise, and how these emotions ultimately determine whether consumers stay engaged or disengage entirely, as other studies have shown that complex financial information environments can generate cognitive overload that translates into emotional strain and avoidance behaviours during decision making.

Research by da Silva Cezar and Maçada (2023), for example, demonstrates that when financial content becomes dense or difficult to process, users experience heightened anxiety and reduced perceived control, which in turn lowers engagement and increases reliance on shortcuts rather than careful evaluation. Their findings reinforce a growing body of behavioural finance literature indicating that disclosure design does not only influence comprehension outcomes but also shapes emotional responses that directly affect trust, persistence, and the quality of consumer decisions.

Most of us approach a credit card agreement with the same quiet dread we reserve for tax forms and instruction manuals. We know it’s important. We’d like to be diligent. But somewhere between the first dense paragraph and the fifteenth undefined term, our attention frays, our pulse ticks up, and a subtle sense of unease takes hold.

This isn’t just a comprehension problem, it’s an emotional one. Our study of consumer reactions to two agreements - Nationwide (publicly available and access date January 2025) and Jaja (publicly available and access date March 2025). It shows that design and language don’t merely influence what people know, they also shape how people feel while reading. This in turn governs whether they stay engaged, what shortcuts they take, and how confident they are in the choices they make.

This allows us to create an emotional map of that experience: where anxiety starts, how stress builds, why distrust spikes, and what to change if we want agreements to empower rather than exhaust. It highlights how these issues directly lead to disengagement, coping mechanisms, and a lack of understanding.

The Cognitive Cost of Complexity: Anxiety in the Reading Experience

Participants engaged in a structured reading and labelling task:

- They each reviewed credit-related texts and marked segments according to their experienced cognitive impact.

- Emotional responses were treated as indicators of mental load and comprehension rather than purely affective states, allowing the analysis to capture moments where complexity disrupted understanding.

- While reading, users identified the category that most closely matched their experience, with flexibility to introduce alternative descriptors if predefined labels felt insufficient.

- After labelling, they rated the perceived intensity on a five-point scale ranging from barely noticeable to overwhelming, enabling the study to quantify how linguistic features, such as dense terminology or legalistic phrasing, shaped cognitive strain during exposure to the material.

Cognitive Strain

These structured responses provide a measurable basis for examining how specific linguistic features translate into heightened cognitive strain.

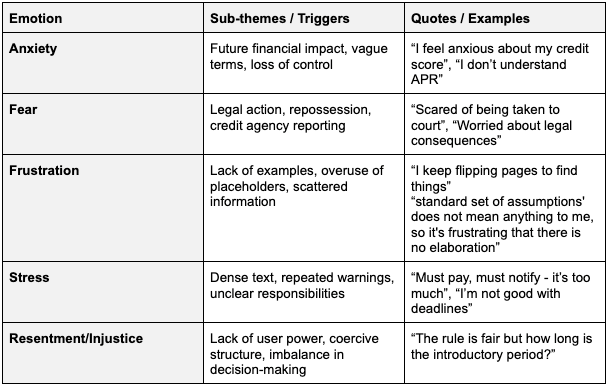

Anxiety was the baseline mood. It flared earliest around unfamiliar or under-explained concepts such as “APR”, “effective rate", " persistent debt”, and intensified when those terms appeared inside long, clause-heavy sentences.

Readers described a mental fog setting in: the kind of fatigue that makes rereading feel both necessary and futile. Nationwide’s more legalistic style amplified this, with several participants calling the experience stressful, overwhelming, or intimidating.

Cognitively, this is classic overload. Working memory gets swamped by jargon, cross-references, and conditional clauses, leaving too little capacity for meaning. As a result, even motivated readers gave up, stating they felt “nervous” or “powerless” because they could not fully decode the text.

“I had to look up compound interest elsewhere.”

“I feel nervous because I can’t tell what APR actually means for me.”

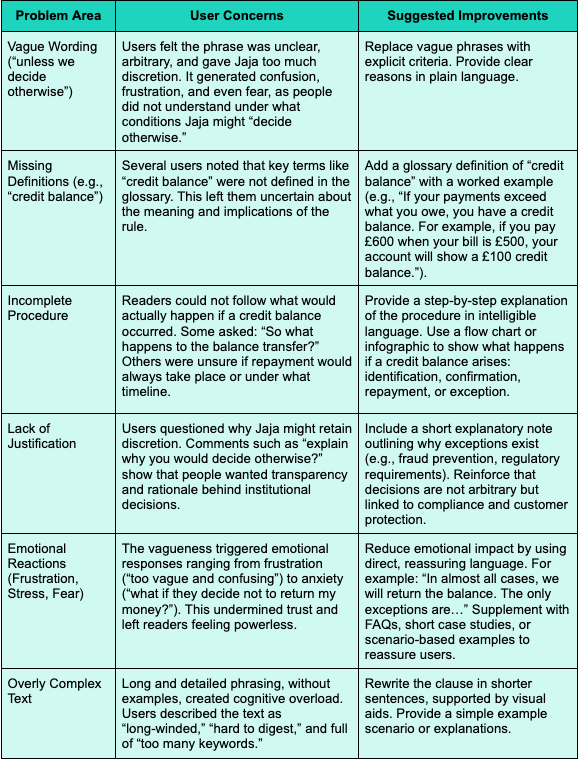

When Uncertainty Feels Dangerous: The Emotional Cost of Vagueness

Anxiety and fear were the most frequent emotional responses across both Nationwide and Jaja. These were triggered by future uncertainty, vague clauses, and perceived loss of control.

Key drivers included:

- Consequences of missed payments, which raised fears of legal proceedings, repossession, or long-term credit damage.

- Ambiguity around terms such as APR or “any other valid reason,” which left users fearing arbitrary changes by the provider.

- Risk of debt spirals, with compounding interest described as a “black box” that participants struggled to calculate or predict.

Quotes such as “I’m worried I’ll end up in debt without realising it” and “They could give examples that would demystify these reasons” underline the close link between unclear language and consumer anxiety.

Decision Pressure Without Tools: Stress at the Point of Action

Emotional stress increased when we asked participants to use the information to make hypothetical decisions. Testing in this way is important in light of the Consumer Duty’s express aim to enable consumers to make ‘informed decisions’.

For example, calculating the cost of missed payments or predicting how fees would accumulate often left users worried about making mistakes. One participant said, “I’m not good with deadlines, and this feels like a trap.”

This stress reflects a deeper problem: credit agreements are not designed as decision-support tools. They present rules and conditions but fail to equip users with practical strategies or examples. The result is that consumers often default to coping shortcuts, such as ignoring difficult sections or focusing only on promotional rates, which undermines informed decision-making.

“Feels One-Sided”: Disempowerment and Perceived Injustice

A recurring emotional theme was disempowerment, and lack of trust. Clauses that gave broad discretionary powers to providers, such as “we may cancel your card at any time for any valid reason,” triggered strong negative reactions. Participants described these as “coercive,” “unfair,” or “one-sided,” with some expressing outright distrust in the fairness of the agreement.

“It feels like they can change the contract for almost any reason.”

This sense of injustice matters because it weakens confidence and trust in financial institutions. When consumers perceive the agreement as stacked against them, they become less willing to engage meaningfully with its content. Instead, they skim or avoid reading altogether, increasing the likelihood of misunderstandings.

Emotional Friction, Defined: The Predictable Triggers You Can See Coming

Across both agreements, the same textual features repeatedly produced negative effects:

These are not random, they’re design choices. And they reliably generate anxiety, fear, frustration, stress, and resentment.

How It Feels in Practice: Two Clauses, Two Profiles

Case A : Nationwide Sample Text

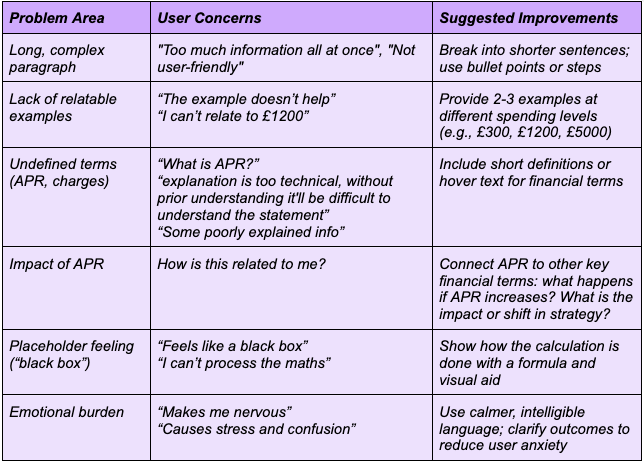

“The total amount payable shows you how much you would repay in total if your credit limit was £1200… you made a £1200 purchase as soon as your account was opened… repaid in 12 equal monthly instalments… assumes the Standard Rate for Purchases applies… interest rate does not change… both you and we keep to the terms… The APR is also calculated on this basis.”

Case B : Jaja Sample Text

“If a balance transfer or money transfer results in a credit balance, we may (unless we decide otherwise) return the full amount of the transfer to the account the money came from.”

What the Agreements Reveal: When Efforts to Inform Create Confusion

Across both Nationwide and Jaja’s credit card agreements, a clear paradox emerged. Documents designed to inform consumers often left them more confused, anxious, and disengaged.

Nationwide’s agreement clearly shows how a compliance-driven approach can overwhelm readers. Its long, densely packed paragraphs and legalistic tone created cognitive overload, while technical details were presented without the clarity or relatable context consumers needed to understand them. A worked repayment example intended to aid comprehension instead felt arbitrary and detached from real financial scenarios. Readers could see the outcomes such as “total amount payable” but not the reasoning behind them. The absence of definitions for core terms such as Credit Limit and charges turned the text into what many described as a “black box.”

The emotional impact was striking. Up to two-thirds of participants flagged parts of Nationwide’s text as stressful or confusing, particularly where the document combined numbers, ambiguous conditions, or discretionary powers like “unless we decide otherwise.” These same sections also corresponded to the lowest comprehension scores. Anxiety, fatigue, and mistrust were not side effects of misunderstanding but rather the cause.

Readers responded defensively: skimming, re-reading without clarity, or giving up entirely. Over time, this emotional burden undermined the agreement’s purpose, discouraging engagement and leaving consumers vulnerable to poor decisions and persistent debt.

Jaja’s agreement (certified with the Crystal Mark and clarity approved by Plain English Campaign) took a different path, replacing formal density with a friendlier tone and simpler design. The agreement is part of an online journey that is certified under the Plain Numbers Mark (a formal seal showing it meets defined clarity standards), Plain Numbers states that its certified journeys have been deployed at scale and experienced by many millions of users, underscoring the practical reach of this standard.

Yet While this reduced initial fatigue, it introduced a different kind of strain.

Several sections triggered strong negative emotions, often because vague or sweeping clauses left users feeling powerless.

For example, clauses stating that providers could refuse balance transfers “for any reason,” or increase charges “at any time,” created a perception of arbitrary control. The lack of clear definitions for terms such as “cash advances” or “compound interest” produced the same anxieties reported with Nationwide’s more formal text.

The plain language approach that made Jaja’s agreement approachable also made it ambiguous, leaving readers uncertain about rules and outcomes.

Together, these cases reveal the same structural flaw: credit card agreements are written with compliance in mind, not comprehension. The same type of powers protecting the rights of the firm, but described in two different but similarly unhelpful ways.

Nationwide’s precision intimidates; Jaja’s simplicity obscures. Both lack the emotional intelligence needed to help consumers feel secure and informed. They present obligations without reassurance, data without context, and rights without clarity.

For true transparency, financial agreements need to go beyond just readable sentences and consider how people think and feel. Until financial agreements are designed with cognitive clarity and emotional safety in balance, consumers will continue to read not to understand, but to survive.

Why Emotions Belong in Compliance

If we accept that credit agreements are emotional documents, design priorities change. Four principles emerged repeatedly from reader feedback:

Anchor terms where they are presented

Define APR, minimum payment, credit balance, cash advance at first use briefly, in-line and in simple language. Let the glossary be a reference, not a crutch.

Show the maths using a real-life context

Replace black boxes with relatable scenarios: a 3-step worked example, a simple timeline, a “what changes if…?” note. Numbers calm people when they can see them and relate in context.

Bound discretion with criteria.

Swap “unless we decide otherwise” for “except in cases of X or Y (e.g., fraud checks, legal holds).” Name the process and the timeline. A little justification goes a long way.

Prioritise Intelligibility

Shorter sentences and plainer vocabulary, while helpful, do not by themselves make a document intelligible. Intelligibility is the disciplined shaping of structure, sequencing, and explanation so that readers can follow meaning without cognitive strain. It requires a logical narrative: clear progression from premise to implication, explicit links between clauses, and formatting that signals hierarchy and consequence (Ortiz et al., 2024).

When agreements are structured for intelligibility, they function as emotional stabilisers as much as informational artefacts. Predictable layout, transparent reasoning, and contextual examples reduce uncertainty at the point of interpretation. Rather than confronting a dense block of text, readers encounter a guided pathway that clarifies what matters, when it applies, and why it exists. These are not merely stylistic adjustments but behavioural interventions that lower anxiety, reduce perceptions of arbitrariness, and sustain attention long enough for genuine comprehension to occur.

It’s tempting to treat negative emotion as a side effect of reading dense material. Our findings suggest the opposite, and that emotion is central to comprehension.

Anxiety narrows attention. Fear biases interpretation. Perceived injustice erodes trust. Together, these elements compel readers to take what feel like self-protective shortcuts, but which ultimately reduces their ability to make informed decisions.

Credit card agreements exist to inform and protect. They only do that when people can read them without feeling cornered. The path forward is not a choice between simple and legal; it’s a commitment to transparent precision. Consumers need clear terms at the point of need, visible logic behind the numbers, bounded discretion with reasons, and prose that respects the limits of human attention.

Design for compliance alone, and you’ll keep getting what we saw here: readers who care, documents that don’t help them, and a widening gap between what’s written and what’s understood.

Explore more articles