The Language Trap: Why Consumers Struggle to Engage with Credit Card Agreements

When most people receive a new credit card, the excitement of financial flexibility quickly fades at the sight of the accompanying agreement. Pages of dense text and technical terms, all presented as if meant to be read, yet seemingly designed to deter engagement.

Interest rate calculations, legal jargon, and vague or poorly explained examples create confusion, stress, and disengagement. Instead of empowering consumers, these documents often generate mistrust and hinder informed financial decision-making.

But how do consumers actually engage with these agreements? And what role does language play in creating confusion, fatigue and, ultimately, mistrust?

This project, funded by UKFIN+, was a collaboration with Professor Maggie Chen and the Cardiff University research team.

It investigates how 60 users engaged with two major credit card agreements: Nationwide and Jaja, and offers a revealing look at how language complexity shapes engagement.

The agreements also differ in their intended audiences. The Nationwide credit card agreement (publicly available and access date January 2025) is structured for customers who meet specific eligibility criteria such as credit scores, employment status, and spending patterns, reflecting typical underwriting and risk considerations.

By contrast, Jaja’s agreement (publicly available and access date March 2025) is short, conversational and clarity-approved by the Plain English Campaign which means it performed well across standard readability tools and aligns with what the industry currently regards as good practice in consumer-facing text. The agreement is part of an online journey that is certified under the Plain Numbers Mark (a formal seal showing it meets defined clarity standards), Plain Numbers states that its certified journeys have been deployed at scale and experienced by many millions of users, underscoring the practical reach of this standard.

The findings paint a striking picture of readers who want to understand but are systematically hampered by language, structure, and design.

The Reality of Reading: Skimming Through the Maze

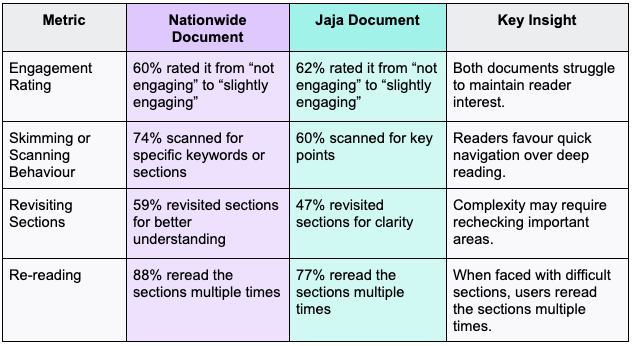

When faced with credit card agreements, consumers rarely engage with text systematically from start to finish. Instead our study found most adopted a fragmented approach: skimming, scanning for keywords such as “fees”, “interest rate”, or “repayment terms,” and revisiting sections only when confused.

For Nationwide, 60% described their experience with the agreement as “not engaging,” while 44% admitted to merely skimming the document. Even Jaja’s mobile-friendly design, with shorter sentences and more white space, only modestly improved engagement: 62% still found it disengaging ( see Table 1).

Across both agreements, over 80% of readers relied heavily on visual cues such as headings, bold text, and bullet points to find what they needed. Full, systematic reading was rare. Only about half of all participants said they read the entire agreement. Most treated these documents less like resources and more like obstacle courses.

The consequences were predictable. Confusion was widespread. Many participants misunderstood fees, timelines, or interest calculations. When asked why, the answers were remarkably consistent: the language was complex, the structure exhausting, and the information overwhelming.

Why Reading Collapses into Scanning

Three major barriers emerged from user feedback: poor information structure, unclear language, and cognitive overload.

1) The information structure itself worked against comprehension. Long paragraphs packed with text, minimal spacing, and few visual aids created a sense of intimidation. Readers described the documents as “visually overwhelming” and “too dense to follow.” Without breaks or guiding visuals, the text became a wall rather than a map.

2) The language alienated readers. Legalistic tones, undefined jargon, and unexplained financial concepts like APR, minimum payment, or total amount payable left users feeling lost. One participant said bluntly: “There’s no definition of APR, or 'effective rates'. It’s unclear what it even means.” Another confessed: “I had to look up compound interest elsewhere just to understand the sentence.”

3) Cognitive overload sets in fast. Even motivated readers described fatigue and the need to “step away” before continuing. Redundant explanations, vague timelines, and long-winded clauses blurred focus. The result was not disengagement born of apathy, but disengagement born of exhaustion.

As an example for Nationwide, users noted:

“Too much information and hard to digest.”

“The example doesn’t provide much certainty, it needs to be fleshed out.”

“Since the sentence involves multiple concepts, I had to look up external resources.”

For Jaja, users noted:

“95% over your credit limit is a bit confusing, I am unsure at this point what a credit limit is and how you can go over this. Maximum limit is not defined.”

“The information is too vague. I am not sure what is meant by the transferred amount that has not been paid off."

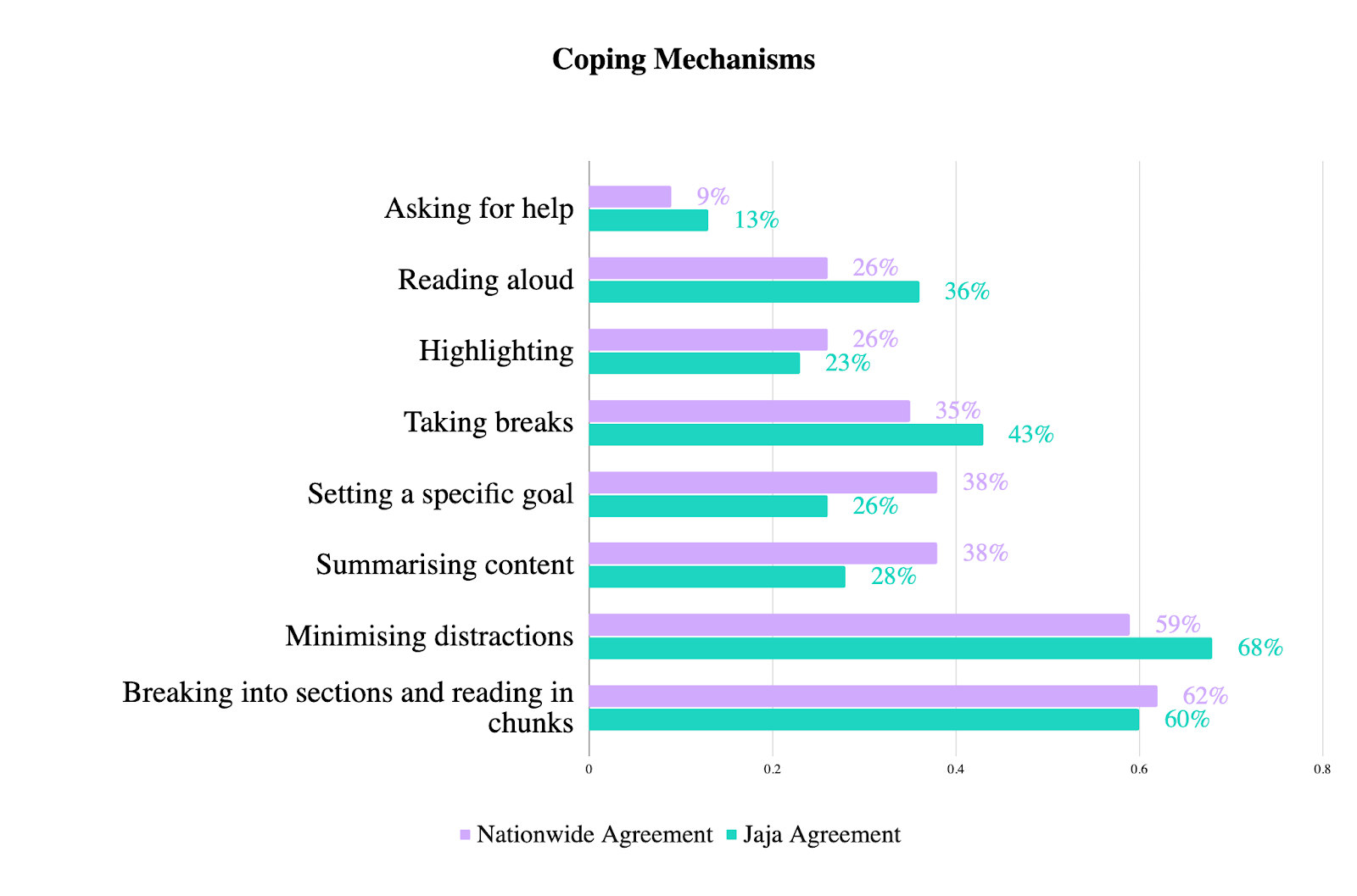

How Consumers Cope: Navigating Credit Agreements Under Pressure

When language becomes a barrier, people adapt (Su & Guo, 2024). Readers of both the Nationwide and Jaja agreements developed coping strategies - not to understand every detail, but to manage their experience.

The most common techniques were breaking the text into chunks, minimising distractions, and summarising key points mentally. Some highlighted, others read aloud, but very few asked for external help. Fewer than 15% sought clarification from others, relying instead on guesswork and intuition.

This behaviour aligns with Cognitive Load Theory - when working memory is overwhelmed, people resort to shortcuts. Similarly, Dual Process Theory suggests that under pressure, people shift from deliberate reasoning to fast, intuitive judgments. The outcome? Readers feel like they’ve “read enough,” when in fact their understanding remains shallow.

The agreements, in effect, teach people to skim rather than to learn.

When Words Work Against Understanding

Language emerged as the single most significant factor shaping engagement.

Nationwide’s text was dense and formal, full of subordinate clauses and legal hedging (“where applicable”, “we may”). Jaja’s style, by contrast, was conversational but vague - despite being easier to read it left gaps. As one user, having read Nationwide explained: “The sentence involves compound interest, average daily balance, unpaid interest… I had to look it up elsewhere.” .

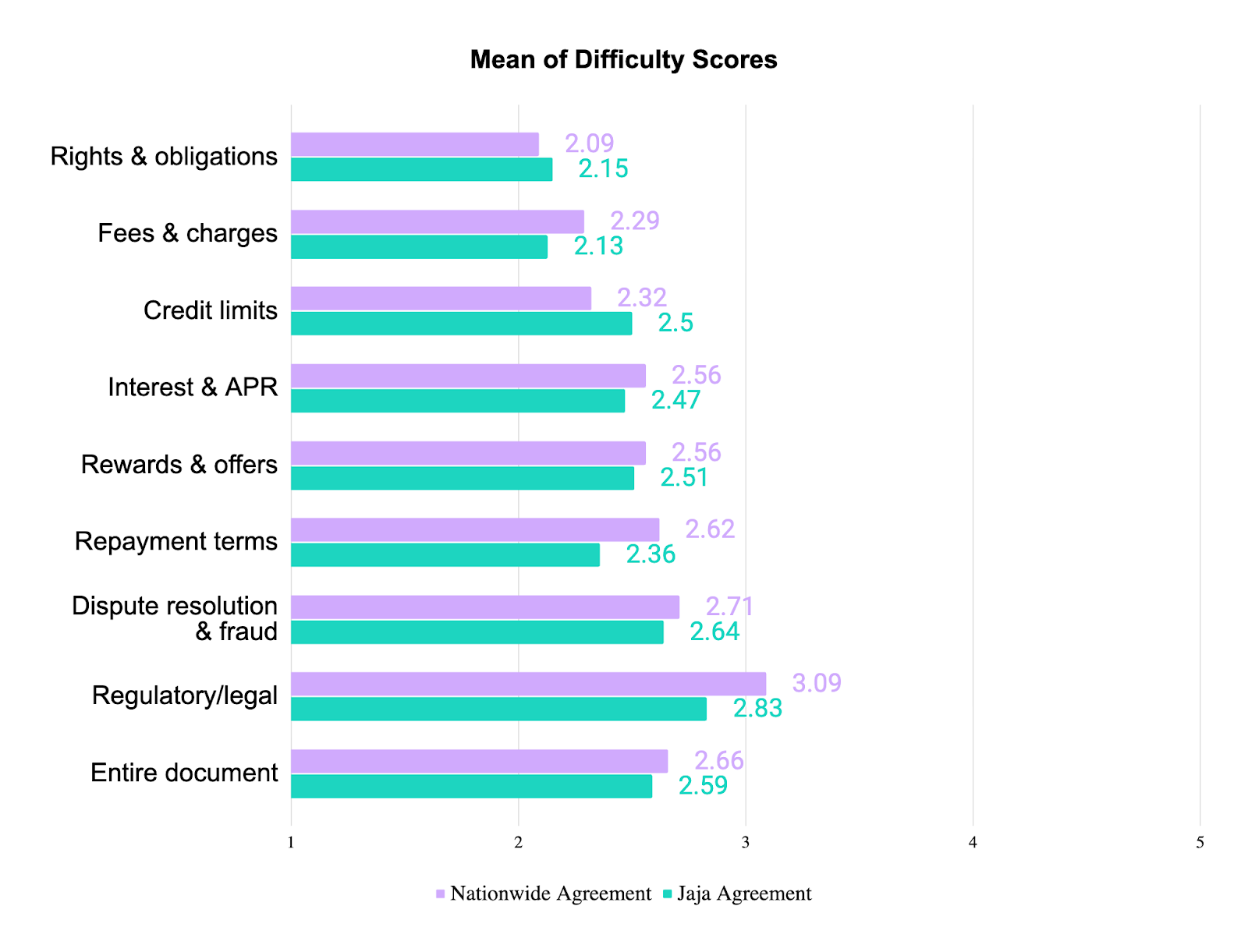

The perceived complexity of the credit card terms was confirmed by user difficulty ratings. On a scale of 1 to 5, with 5 indicating the maximum difficulty, users assessed how challenging it was to understand the concepts presented in the agreement.

Regulatory and legal sections were the hardest in both agreements (Nationwide 3.09, Jaja 2.83), while rights and obligations and fees were somewhat easier. Overall averages were nearly identical (Nationwide 2.66, Jaja 2.59), showing that despite stylistic differences, neither agreement achieved accessible clarity.

In other words, the choice of style - whether intense or informal - mattered less than one might expect. Whether heavy-handed or overly casual, neither approach achieved genuine clarity.

Dissecting the Language Barriers

Behind this broad struggle lay several distinct linguistic challenges.

1. Terminology and Conceptual Barriers

A consistent barrier across both agreements was the difficulty users faced in understanding core financial terminology and concepts. Terms that are central to credit card use, such as APR, compound interest, and minimum payment, were often either undefined, vaguely referenced, or explained in ways that assumed prior knowledge.

Participants highlighted this gap:

“What’s the difference between simple standard rates and effective rates?”

“I don’t get how you go from APR to a monthly payment. Is there a formula or something?”

“No clear definition of 'Total Amount Payable'.”

Vocabulary and Jargon

Specialised terms like “APR,” “effective rate,” and “compound interest” were repeatedly flagged as confusing. Users expressed frustration when these concepts were introduced without definition or context. One noted: “Domain specific concept – APR.” Another added: “Too many terms and few examples making it hard to understand.” Without worked examples or simple explanations, these terms left users uncertain about the most basic mechanics of borrowing.

Sentence Structure

Even when terms were familiar, the way they were embedded in text created additional barriers. Long sentences packed with multiple clauses or vague references increased cognitive load, forcing readers to slow down or re-read.

Comments included: “Long sentences, the use of ‘this’ without stating clearly what ‘this’ is.” Another user explained: “The sentences are too long and convoluted.” Such structures made it difficult to extract key information or follow logical steps in calculations.

Implicit Information

In several cases, agreements referred to assumptions or standard practices without actually explaining them. This created what users described as a “black box” effect, where outcomes like APR appeared without clarity on how they were derived.

As one user observed: “It’s a linguistically simple sentence, but it doesn’t actually explain how they calculate APR.”

Another said: “This section assumes understanding of interest, charges, and Standard Rate of Purchases.”

In practice, these omissions left readers guessing at the logic behind the numbers.

The combined effect of jargon, convoluted sentences, and hidden assumptions is that consumers are left with partial recognition but little functional understanding of the very terms that determine their borrowing costs. Agreements transmit information but do not teach. As a result, users feel both overwhelmed and under-informed, able to repeat the vocabulary but not apply it to real financial decisions.

2. Lack of Contextual Anchoring

Many users highlighted that they wanted definitions to be embedded within the flow of reading, rather than at the end or in a glossary. Furthermore, there was limited contextualisation; terms were not linked to real-life outcomes, reducing users' ability to apply them practically.

Examples for Nationwide:

“This sentence contains many terms and they are very important to using credit card, I need look up sources like external website and examples for better understanding.”

“Uses a lot of terminology which had not been explained in enough detail in the above sections which means that it takes a lot of re-reading to comprehend what the example is supposed to be showing.”

Examples for Jaja:

“What is the minimum payment?”

“Define simple interest with example.”

3. Missing Examples and Visualisation

Users repeatedly requested worked examples, timelines, and step-by-step breakdowns. Without these, abstract concepts like “penalty”, “interest” or “balance transfers”, remain vague. The absence of tables, diagrams, or visual aids was a notable weakness in all documents.

Nationwide:

“Information is far better suited for a table with examples included.”

“An infographic explaining compounding and interest would be much more beneficial and comprehensible.”

“Case study would help illustrate what they mean by compounding.”

“Could use a concrete example, and could also include what is actually laid out in the Tariff of Charges.”

“I think a link to example promotions would help me understand this provision.”

Jaja:

“Explaining what this process means would be very helpful, either by linking to external sources or generating a simple infographic.”

“Visual aids or infographics could show this information”

4. Structural and Syntactical Overload

Long sentences packed with multiple conditions or clauses increased cognitive strain. Passive voice and legal hedging (e.g. “we decide”, "we can") caused ambiguity and forced users to re-read sections multiple times. This effect was strongest in Nationwide credit card agreement .

5. Emotional Tone and Language Framing

Even ostensibly neutral language sometimes conveyed negative implications. Words like monitor, decline, or legal action were described as intimidating, especially when presented without accompanying guidance. Tone significantly influenced perceived fairness and trustworthiness of the documents.

Different Styles, Same Struggles

Despite their stylistic differences, both Nationwide and Jaja revealed the same underlying problem: the tension between simplicity and precision.

Nationwide’s dense, legalistic text aimed for precision but lost readability. Jaja’s friendly tone invited engagement but sacrificed accuracy. As one reader put it, “Nationwide overwhelms, Jaja under-explains.” The result was a double bind, one intimidating, the other vague.

Both approaches, ultimately, left consumers uncertain about key terms and unable to act confidently. The lesson here is not that simplicity alone solves the problem, but that effective understanding requires both precision and accessibility.

The Transparency Gap: What Consumers Really Want

Across all feedback, one theme echoed loudly: a demand for transparency. But transparency, for consumers, means more than readable English. It means understanding how terms are defined, how charges are calculated, and when or why conditions might change.

The latest Draft Guidance on Unfair Contract Terms released by the CMA makes this clear. Transparency is determined by whether the information can be understood in practice. It needs to be intelligible, easy to navigate, well structured and the key points made both prominent and understandable.

In our test, many participants expressed frustration with vague or open-ended language. Phrases like “for any valid reason” or “standard set of assumptions” struck them as loopholes. “It feels like they can change the contract for almost any reason,” one respondent said. Others were annoyed by cross-references to future sections or undefined jargon like “total balance the installment plan covers.”

Even examples intended to clarify often missed the mark. Some were too simplistic to be useful; others so complex they made matters worse. What users wanted were clear, worked scenarios, or even interactive tools, something that would turn abstract percentages into tangible consequences.

The emotional dimension was equally important. When agreements used intimidating phrasing or appeared to conceal information, users felt powerless. “Feels unfair,” said one reader. “Lack of control,” said another. In this sense, opacity was not just a cognitive barrier but a psychological one.

The Bigger Picture: When Design Meets Decision-Making

The findings tell a consistent story - a number of factors form a self-reinforcing cycle:

- Engagement - how deeply readers connect

- Barriers - obstacles that disrupt understanding

- Coping - strategies readers use to manage confusion.

Structural and linguistic complexity pushes readers toward shallow engagement. In turn, shallow engagement limits understanding and trust. And without trust, even clear sections are read with suspicion.

Consumers don’t stop reading out of disinterest, they do so because it’s a rational response to poor design and information overload. When faced with dense or confusing material, people conserve effort by skimming, scanning, guessing, and moving on.

For financial providers, this presents a serious challenge. Plain language and readability alone isn’t enough.

Genuine transparency in documentation demands a blend of clarity, context, and justification. Simply being brief can be as unhelpful as being overly verbose. To achieve this, key terms should be defined where they appear, the rationale behind charges should be explained, calculation methods should be demonstrated, and the implications of actions should be illustrated with realistic examples.

Rethinking Financial Communication

The implications extend far beyond credit cards. As financial products grow in complexity, the ability of consumers to make informed choices depends increasingly on how clearly those choices are communicated. Legal compliance does not equal comprehension.

In both the Nationwide and Jaja agreements, the least understood sections were the very ones regulators insist must be transparent. Despite meeting disclosure requirements, they failed in their practical goal: to be understood.

To fix this, providers and regulators must move beyond surface readability and toward intelligibility. The language of finance should empower, not exhaust. It should reduce anxiety, not amplify it. And it should treat consumers not as liabilities to be protected from misunderstanding, but as participants in a conversation about value, responsibility, and trust.

The irony is striking: credit card agreements are meant to inform consumers about their rights and responsibilities, yet their language often prevents precisely that. Nationwide’s density and Jaja’s vagueness represent two sides of the same coin: documents written for compliance, not comprehension.

Consumers today are not passive readers. They are active information seekers operating under cognitive constraints. When financial text ignores this reality, it alienates the very people it is meant to serve.

Financial communication achieves real intelligibility only when clarity transcends compliance and becomes an ethical commitment and a form of respect for consumer understanding.

Explore more articles