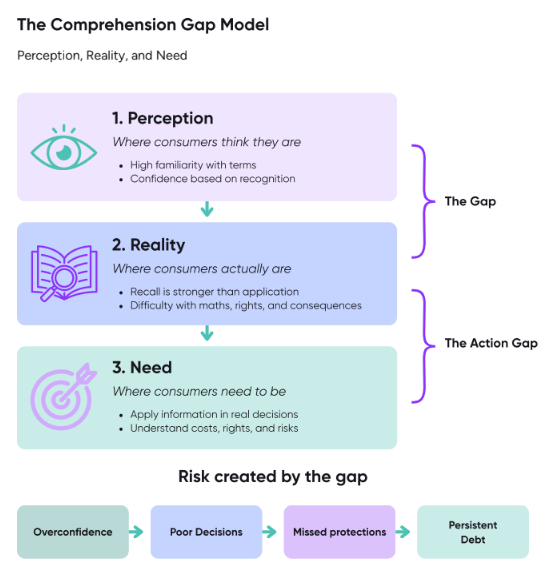

The Comprehension Gap: Perception, Reality, and Need

Research summary

What Amplifi Multi-Level Comprehension Framework tells us: The Comprehension Gap Model: Perception, Reality, and Need

Credit card agreements are meant to help consumers understand the products they are entering into. They should explain the cost of borrowing, the consequences of repayment choices, the user’s rights, and the obligations attached to the agreement.

In practice, these documents often create a different outcome. Consumers may recognise the language used in credit card agreements but they still struggle to apply that information when making financial decisions.

Our study was a collaboration with Professor Maggie Chen and the Cardiff University research team and was funded by UKFIN+. It explores the problem of consumers failing to understand credit agreements through the Amplifi Multi-Level Comprehension Framework©. Used by the Financial Conduct Authority (FCA), it assesses understanding across different levels: from basic recognition and recall through to inference, application, reflection, and action.

The findings show that the central issue is not simply that consumers lack knowledge. Rather, many consumers experience an illusion of familiarity. They feel confident because they have seen terms such as minimum payment, APR, credit limit, and interest rate before. But recognising them does not mean they can then use those concepts to calculate costs, compare products, understand risk, or act on their rights.

Familiarity and understanding are very different, but it seems often confused.

This distinction matters because credit card agreements are not just documents to just share information. They are decision-making tools. A consumer does not only need to know that a minimum payment exists. They need to understand how paying only the minimum can extend repayment time, increase the total amount paid, and contribute to persistent debt. They do not only need to recognise APR as a familiar term. They need to understand how they use it to compare similar products and how it affects the cost of borrowing.

The research points to a structural problem in consumer understanding.

Users enter the agreement process believing they understand enough, but the agreement often does not help them move from surface-level familiarity to practical comprehension. Dense wording, fragmented layout, financial jargon, weak explanations, and limited worked examples all make it harder for consumers to translate information into action.

The Comprehension Gap Model below summarises the core finding of the study: there is a distance between what consumers think they understand, what they actually understand, and where their understanding needs to be in order to manage credit responsibly.

1. Where Consumers Think They Are: Perception

At the perception level, consumers believe they already have a reasonable understanding of credit card agreements. This confidence is partly explained by the familiarity of common financial terms.

In our study, participants rated themselves highly familiar with terms such as minimum payment at 4.15 out of 5, credit limit at 4.12 out of 5, fees and charges at 4.09 out of 5, and interest rates at 4.06 out of 5.

These scores suggest that many consumers do not approach credit agreements feeling completely uninformed. Instead, they often feel that they already know the basics. This may be reasonable. Credit card terminology appears across banking apps, advertising, comparison websites, statements, and everyday financial conversations. Repeated exposure makes the terms feel clear and manageable.

However, this confidence can be misleading. Familiarity with a term is not the same as understanding how that term operates in practice. A consumer may recognise the phrase “minimum payment” but still underestimate the long-term cost of making only that payment. They may know that APR relates to interest, but still struggle to compare the true cost of different credit offers. They may have heard of withdrawal rights or consumer protections, but not know when or how to use them.

This is where the illusion of familiarity begins. Consumers feel informed because the language is familiar, but their understanding remains fragile when the information needs to be interpreted, calculated, or applied.

2. Where Consumers Actually Are: Reality

The Reality Level in the Gap Model shows what happens when their perceived understanding is tested. The findings indicate that consumers often perform reasonably well at basic recognition and recall. For example, many participants could identify the overall purpose of the agreement or remember factual information from the document.

However, their comprehension declined sharply when the tasks became more complex. Participants struggled when they had to interpret meaning, apply information to scenarios, calculate financial consequences, or reflect on the fairness and practical impact of terms. This was especially clear in questions involving financial maths.

Testing the applied level of comprehension exposed one of the most important weaknesses.

Many consumers found it difficult to calculate the effect of interest, understand the consequences of missed payments, assess the long-term impact of minimum repayments, or evaluate whether a promotional rate or balance transfer was genuinely beneficial. This matters because these are not abstract comprehension tasks. They mirror the kinds of decisions consumers have to make when using or applying for credit.

The research also found limited awareness of their rights and obligations. Many participants described themselves as “somewhat aware,” but very few reported being fully aware. This suggests that users may sense they have some understanding, but do not have the detailed knowledge needed to protect themselves in real situations, such as withdrawing from an agreement, disputing a charge, or relying on statutory protections.

In reality, many consumers are not operating at the level required for confident financial decision-making. They can often recognise the agreement’s language, but they cannot always use that language to understand consequences, manage risks, or take informed action.

3. Where Consumers Need to Be: Need

The Need Level represents the standard of understanding required for credit card agreements to serve their intended purpose. Consumers must move beyond recognition and recall. They need to understand the practical consequences of the agreement and use that understanding to make decisions.

At this level, a consumer should be able to:

- understand how repayment choices affect the total cost of borrowing

- recognise how minimum payments can contribute to persistent debt

- estimate or compare the cost of APRs, fees, promotional rates, and balance transfers

- understand the consequences of missed payments

- identify key rights, including withdrawal and dispute protections

- know when and how to act if something goes wrong

- decide whether a product is affordable, suitable, and manageable

This is the level at which consumer understanding becomes meaningful. The goal is not simply that users can repeat terms from the agreement. The goal is that they can use the agreement to make informed choices, avoid harm, and protect their own interests.

The Comprehension Gap Model: Why this Matters

This reveals a double gap.

First, consumer understanding is often below where they think it is. Their confidence is based on recognition rather than applied understanding. They feel familiar with the language of credit, but their understanding breaks down when they need to calculate, compare, interpret, or act.

Second, consumers’ understanding is below where they need it to be. Credit card agreements require practical comprehension because they involve real financial consequences. If users cannot understand repayment costs, persistent debt, fees, rights, and obligations, then the agreement is not functioning as an effective decision-making tool.

This gap creates risks for consumers, firms, and regulators. Consumers may underestimate the cost of borrowing, rely on minimum payments without understanding the consequences, miss important rights or protections, or enter agreements with misplaced confidence. Firms may face increased complaints, disputes, remediation costs, and regulatory scrutiny. Regulators are left with an important challenge: disclosure alone is not enough if the information does not support genuine comprehension.

The implication is clear. Credit card agreements must do more than present information. They must help consumers progress up the comprehension gap from familiarity to applied understanding and informed action. This requires clearer structure, worked examples, scenario-based explanations, better signposting of rights, and practical support for decision-making.

Until that happens, many consumers will continue to sign agreements they can recognise but cannot truly use.

Explore more articles