How ‘Simple’ Credit Card Agreements Leave Consumers Dangerously Unprepared

How ‘Simple’ Credit Card Agreements Leave Consumers Dangerously Unprepared

Credit card agreements are meant to serve two purposes at once. They are at once legal contracts, and information tools that should enable consumers to make informed decisions. On paper, these aims appear aligned. In practice, they often pull in different directions. For many consumers, credit card terms and conditions are still among the hardest documents to use, navigate, and genuinely understand.

Over the last decade, and particularly since the Consumer Duty, the industry has tried to solve this problem by making the surface of these documents more appealing. Firms have introduced friendlier language, modern web and app interfaces, shorter contracts, clearer headings, and more visual cues. Regulatory pressure, from the FCA’s Consumer Duty and impending reforms to the Consumer Credit Act, has forced providers to take this issue more seriously. They have talked about enhancing fair outcomes and consumer understanding. On the surface, there is more colour, more icons, and fewer footnotes.

Industry responses have focused on surface-level improvements: Friendlier language, cleaner layouts, shorter sections, and updated digital interfaces have made agreements look more approachable. Regulatory pressure has amplified this trend, but these changes have not altered the underlying cognitive experience. Readers may face fewer footnotes and more icons, but they still struggle to grasp how the terms relate to the decisions they must make when using credit.

The result is a persistent gap between presentation and comprehension. People want to know what minimum payments actually mean for long-term cost, how promotional periods work when payments are missed, and when their rights apply in practice. These are fundamental questions because credit products shape household finances in lasting ways.

The complexity of credit agreements, demonstrated through research over several years, stems from a combination of factors: their dense legal framework, the inherent difficulty of the concepts, the use of specialised terminology, and numerical detail that is rarely illustrated, day-to-day situations.

When consumers misinterpret how fees or interest operate, the consequences are not minor. Misunderstood terms contribute to prolonged repayment, unexpected charges, and entrenched debt. At scale, this undermines fairness, inclusion, and informed consent.

Why Intelligibility Matters

This landscape forms the context for the FCA’s Consumer Duty and the upcoming reforms to the Consumer Credit Act. Regulators now expect firms to move beyond disclosure. It is no longer enough for documents to be accurate. Providers must demonstrate that consumers genuinely understand what they are signing and can act on that understanding.

The stakes rise further when considering vulnerability and resilience. In the FCA’s most recent Financial Lives Survey, nearly half of UK adults exhibit at least one characteristic of vulnerability, and almost a quarter have low financial resilience. These are not edge cases; they represent millions of people who frequently use credit products. Yet most do not disclose their vulnerability to firms, and few feel encouraged to do so. This means many high-risk users are navigating complex agreements without signalling that they may need additional support, creating an operational and ethical challenge for providers.

In this environment, intelligibility becomes a critical measure. It is not simply a stylistic preference but a legal requirement. Consumers must be able to understand their rights and obligations sufficiently to avoid ambiguity and make informed decisions. Readability is necessary but insufficient. A document can be simple on the page and still fail to convey how a product works in real life.

Amplifi’s intelligibility score assesses the likelihood that different population groups genuinely understand a document. When applied to twelve UK credit card agreements, the scores ranged from the high thirties to around seventy, with an average of fifty-six. Half of the providers fell below that midpoint. Put differently, many agreements are only understandable to roughly half of UK adults. For products widely used by people with lower literacy, lower numeracy, or greater vulnerability, this is a substantive risk.

The evidence suggests that plain language alone will not solve the problem. Credit agreements need to be structured, illustrated, and explained in ways that help consumers integrate information into real decisions. Until firms design agreements to meet intelligibility standards, rather than simply passing readability checks, many consumers will continue to commit to obligations they do not fully understand and take on risks they cannot anticipate.

Aim and Approach of the Study

This study set out to investigate, in depth, the barriers consumers face when reading credit card agreements. Although such agreements are formally intended to inform and protect, the reality is that their density, numerical complexity, and legalistic structure routinely overwhelm users.

This project, funded by UKFIN+, was a collaboration with Professor Maggie Chen and the Cardiff University research team. It goes beyond merely identifying what consumers struggle with; it seeks to uncover the why, capturing the cognitive and behavioural challenges that prevent these agreements from serving as effective decision-making tools.

Ultimately, the goal is to provide deep but also practical insights into how credit card agreements can be redesigned to empower consumers to move, from simply recognising terms, to confidently understanding and acting upon them.

The findings will inform new approaches to make financial contracts more comprehensible, fair, and inclusive, predicting whether documents are genuinely accessible across diverse user groups.

Jaja as a Fintech Case Study

Jaja’s digital-first credit card provided a useful test case within the broader research. The product is positioned as a departure from traditional banking, and its agreement reflects that intent. It is short, conversational, certified with the Crystal Mark and clarity approved by Plain English Campaign, and performs well across standard readability tools. By conventional measures, it represents what the industry currently regards as good practice.

A deeper assessment produced a different story. Amplifi recorded an intelligibility score of 54 out of 100, well below the recommended minimum benchmark of 70 for firms aiming to meet regulatory expectations on consumer understanding and Consumer Duty. Reach estimates further sharpened the concern. Traditional readability tools suggested that almost all readers would be able to consume the agreement without difficulty. Amplifi’s results suggested that only about half of UK adults could genuinely understand it, falling to roughly one third among more vulnerable consumers.

The comparative table highlights this divide. Jaja excels on every familiar readability measure and appears to offer a model of accessible communication. The agreement on the surface looks simple, reads smoothly, and satisfies established readability criteria, however intelligibility scores reveal a key difference. The score also indicates that individuals who are not native English speakers would likely struggle more to understand the content.

Table 1. Comparison of industry measures with Amplifi Intelligibility scores

The Amplifi Multi-Level Comprehension Framework: Identifying Where Understanding Breaks Down

We employed the Amplifi Multi-Level Comprehension Framework to analyse how a sample of 47 participants understood and applied Jaja’s agreement. The Amplifi Multi-Level Comprehension Framework is a dynamically structured, purpose-built framework for assessing how well consumers understand information, such as legal and financial communications. Unlike traditional methods that rely on simple recall, Amplifi evaluates comprehension across a number of levels. Each of these levels maps to real-world tasks the user must perform, such as interpreting consequences, making informed decisions, or taking action. The framework is flexible and tailored to the purpose of each document. It is designed to practically and objectively measure comprehension. It is especially valuable in regulated sectors where understanding affects consumer outcomes and compliance.

This framework is customised to assess comprehension across six levels:

- Main (Purpose Recognition): Could the participant identify the overall purpose of the agreement?

- Basic Recall: Could they remember specific facts ?

- Inference: Could they interpret meaning, for example, why a clause exists or what it implies?

- Applied: Could they apply the information to a practical scenario, such as understanding the cost of borrowing?

- Reflection: Could they think critically about the relevance, fairness, or clarity of terms?

- Action: Could they demonstrate confidence in making a financial decision based on the agreement?

Key Insights of Amplif’s Framework

Each participant completed comprehension questions mapped to these six levels. Scores were then expressed as the percentage of participants who answered correctly or appropriately at each level.

The results for Jaja agreements reveal a consistent pattern: strong performance at the top levels of recognition and recall, as 84% of participants correctly identified the main purpose of the agreement, this was then followed by a steep decline once users are required to interpret, apply, or act on the information.

As tasks progressed from basic recall to inference, applied, and reflection, comprehension deteriorated significantly. Less than half could apply the information to real-life scenarios, such as calculating penalties for missed payments.

Figure 1. Amplifi Multi-Level Comprehension

The results for Jaja revealed a consistent pattern:

1. Basic-Level Recall is Common but Misleading

At the level of main purpose, performance was relatively strong, where 84.78% of participants correctly identified the main purpose of the agreement. Most participants could identify what the document was about and describe its broad function.

This “memory game” is enhanced by design features such as familiar fonts, well-structured sections, or repeated terms that make documents easier to scan. While this improves recall, it does not improve comprehension. In fact, it can give consumers the impression that they understand more than they really do. At this level, 59.78% of participants correctly responded to the questions.

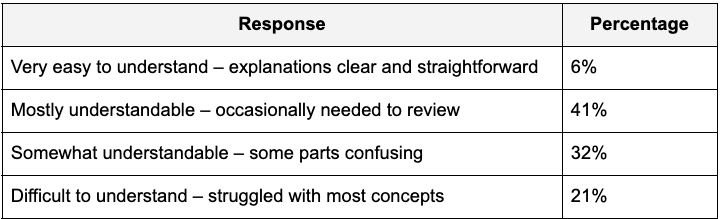

2. Major Deficits in Applied Level: The Maths Problem

While 41% of users found the mathematical concepts in credit agreements to be mostly understandable, only a small minority (6%) rated them as very easy to understand. Strikingly, about one-fifth (21%) of users admitted to struggling with most of these concepts.

Table 2. Accessibility and Understanding of Mathematical Concepts in Credit Agreements

Only 39.49% of participants correctly responded to the applied questions.

Participants struggled with calculating monthly interest, estimating repayable amounts under different payment strategies, or understanding how balance transfers interact with purchases. Many misunderstood how behaviours such as making only the minimum payment or missing a due date would impact their long-term financial outcomes.

This difficulty is consistent with a broader body of research on financial literacy, which has long shown that many adults find compound interest, debt accumulation, and risk diversification challenging. Credit card agreements require users to apply exactly these kinds of skills. They must interpret and calculate interest on outstanding balances, understand the difference between paying in full and paying the minimum, and anticipate the cost of cash advances or balance transfers.

3. Comprehension Declined with Increased Complexity

True comprehension requires more than remembering facts; it requires reflection and action. Our results show that less than half of participants ( 40% for reflection and 28%) were able to correctly reflect and act on the information, such as :

- As tasks progressed from basic recall to inference, applied, and reflection, comprehension deteriorated significantly.

- While most users could restate a clause, a few could explain its practical implications or predict outcomes.

- When asked about consequences such as cost of borrowing or compounding interest, correct answers fell to 15–20%.

- On high-stakes, judgment-based questions, fewer than 30% of participants provided complete and accurate responses.

While users grasp surface-level facts (e.g., repeating clauses, citing interest rates), their understanding collapses when applying this to their personal finances and future decisions. They are relying on memory, not informed judgment.

The agreements' structure worsens this problem. Key financial and legal terms are often undefined, vaguely explained, or use technical language, and concepts (e.g., interest rates, minimum payments) are presented in isolation without explaining how they interrelate. Definitions, if present, are often decontextualized.

Participants repeatedly noted that technical language appeared without support, forcing them to look for external resources. They wanted definitions embedded at the point of use, not tucked away in a glossary. They asked for reminders of key concepts and for more explicit explanations that tie terms to real-life examples. They also called for more intuitive digital tools, such as glossaries accessible via hover or tap, that could allow them to revisit definitions without breaking the flow of reading.

Towards a New Intelligibility Standard

Jaja’s agreement reflects the industry’s most common interpretation of progress: shorter text, cleaner design, and friendlier tone. These changes make documents less intimidating, but they do not solve the central problem identified throughout this study.

Under the Consumer Duty, firms are expected to ensure that customers can genuinely understand and act on key information. Jaja’s agreement shows how far the industry still is from meeting that bar. Its accessibility on the surface does not translate into the deeper intelligibility required for sound financial decisions.

A meaningful standard of intelligibility requires a shift from presentation to cognition. The question is no longer whether a document is easy to read, but whether it supports the user in building a functional mental model of how the product works. That requires movement across the comprehension ladder: from recognition, to interpretation, to the applied understanding needed to manage credit safely.

This progression needs to be designed with intention. Agreements should do more than list terms; they should help people see how those terms fit together in real life.

Consumers need to understand how minimum payments keep interest accumulating, how promotional rates interact with everyday spending, and how a single missed payment can reshape the whole repayment path. The goal is to help users anticipate what will happen next, not rely on guesswork or familiarity with financial jargon.

Meeting this standard means rethinking agreements from the ground up.

Instead of documents built mainly for disclosure, we need documents built for decision-making. That means placing definitions exactly where readers need them, using short and concrete examples to show how rules work, and building scenarios that mirror what people actually do, such as paying only the minimum or mixing purchase and promotional balances. Visual elements can make timelines and cost patterns immediately clear, turning abstract written ideas into something tangible and more engaging.

Even the most familiar terms need this treatment. Phrases like minimum payment or cash advance feel obvious to many people, but their real implications only become clear when tied to concrete, everyday situations. Digital formats offer even more opportunity by letting users expand sections for extra detail, test simple scenarios, or see personalised illustrations without breaking their reading flow. This is what a more helpful, consumer-focused credit agreement should aim to deliver.

This redesign must be paired with outcome-based measurement. Readability tests cannot detect whether users can carry out calculations, connect related clauses, or identify consequences. Tools such as Amplifi’s intelligibility scoring and multi-level comprehension framework are helpful to reveal whether different population groups can understand and apply the information in practice.

Until the industry adopts an intelligibility standard anchored in applied understanding, modern agreements will continue to offer the appearance of clarity while leaving many users exposed. Jaja’s agreement demonstrates this gap vividly. It is polished and approachable, yet it leaves a significant proportion of readers confident but unequipped. This creates precisely the risks that regulatory reforms are intended to eliminate.

Jaja’s document is therefore not just an example of contemporary fintech design. It is a signal to the wider market. Simplicity that lacks depth does not protect consumers. It creates the conditions for misunderstanding, overconfidence, and long-term financial harm.

A new intelligibility standard is needed to ensure that credit agreements function as genuine tools for informed, safe, and fair financial decision-making.

Explore more articles